The global energy landscape heading into 2026 is defined by a profound structural contradiction. On one side stands the “OPEC+ Squeeze”—a multi-year effort to artificially constrain supply and defend a price floor. On the other stands the “Super Glut”—a tidal wave of non-OPEC production combined with demand destruction in China that has overwhelmed the cartel’s interventions.

Translating these colliding forces into a granular impact assessment for Malaysia reveals a historic decoupling: a nation historically tethered to oil revenues is now seeing its currency strengthen even as its petroleum income falters. The historical Pearson correlation coefficient between Brent Crude and the USD/MYR pair has collapsed from a 5-year mean of +0.68 to a statistically insignificant -0.12 in late 2025. This breakdown in the “Petro-currency” beta is evidenced by a 7% year-to-date appreciation in the Ringgit despite a 25% contraction in benchmark crude prices. This suggests that MYR’s price action is now driven by non-commodity factors, specifically the narrowing of interest rate differentials and high-conviction FDI inflows into the semiconductor and data center sectors.

1. The OPEC+ Squeeze

The “OPEC+ squeeze” refers to a tiered system of production curtailments intended to drain global inventories and sustain crude oil prices above the fiscal breakeven levels of member states, typically targeting the $80 per barrel range. As of late 2025, this strategy has removed approximately 5.86 million barrels per day (mb/d) of potential supply from the market, representing roughly 5.7% of global demand.

The squeeze operates through two primary mechanisms:

- Mandatory Quota Reductions: Official production targets set for all Declaration of Cooperation (DoC) members, recently extended through December 2026.

- Voluntary Cuts: Additional, unilateral reductions by eight core members (Saudi Arabia, Russia, Iraq, UAE, Kuwait, Kazakhstan, Algeria, and Oman). These include a 1.66 mb/d cut extended through 2026 and a more transient 2.2 mb/d cut that the group has struggled to unwind.

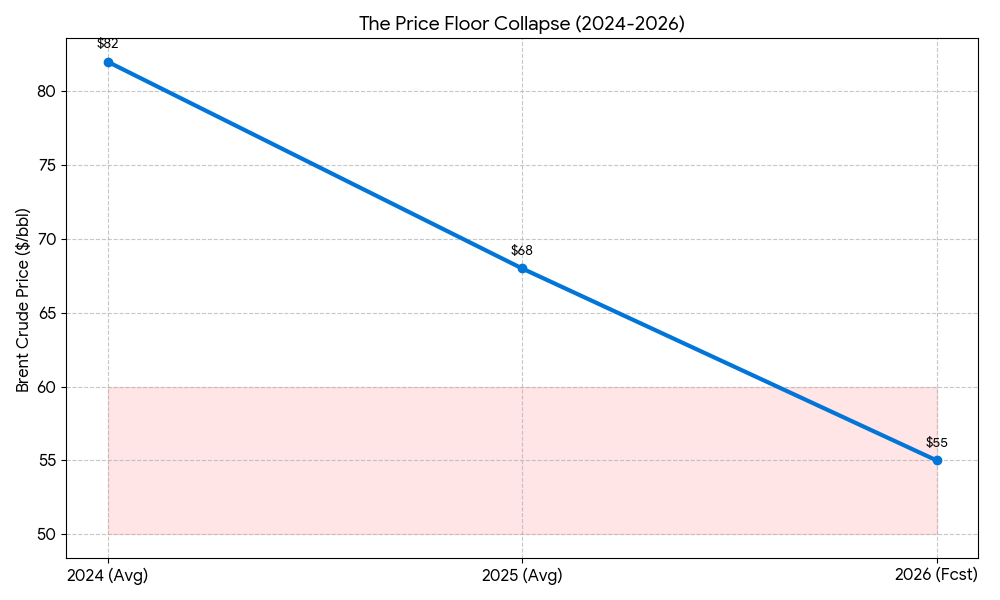

Despite these aggressive interventions, the squeeze has largely failed to achieve its price objectives in 2025. Benchmark prices for Brent Crude and West Texas Intermediate (WTI) have decoupled from the geopolitical risk premiums that characterized 2022-2023, collapsing to the $60–$63 range by December 2025, with forecasts pointing toward a $55 floor in 2026.

The market’s reaction indicates a shift in sentiment from “scarcity fear” to “surplus realization.” Traders have begun pricing in a structural overhang, driven by the realization that OPEC+ is essentially subsidizing its competitors. By keeping prices artificially elevated (or attempting to), the cartel has incentivized high-cost production in the United States, Brazil, and Guyana, while simultaneously accelerating demand destruction via electrification in China. This phenomenon has forced OPEC+ into a defensive “wait-and-see” posture, delaying the unwinding of cuts to avoid triggering a total price collapse.

2. Global Supply and Demand Architecture: The Widening Imbalance

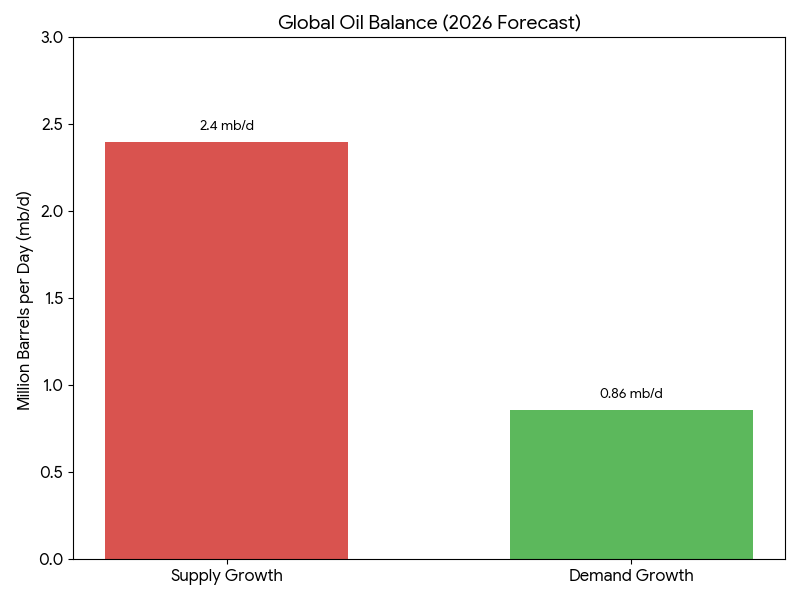

The failure of the OPEC+ squeeze to sustain prices is not merely a cyclical downturn, but the result of a fundamental structural realignment in the global energy market that has neutralized the cartel’s historical leverage. This shift is characterized by a “widening imbalance” where the aggressive expansion of non-OPEC producers—dubbed the “Rise of the Americas”—has fundamentally reshaped the supply side of the equation. Spearheaded by the United States, which achieved a record output of 13.84 mb/d in 2025, this surge is not the result of frantic drilling but rather a “manufacturing mode” of operational efficiency within the Permian Basin. By allowing producers to extract higher volumes of oil with fewer rigs, this efficiency has permanently lowered the marginal cost of production, while simultaneous capacity expansions in Brazil and Guyana have further tipped the scales. Consequently, the non-OPEC share of global supply has climbed from 38% in 2015 to an estimated 52–55% today.

On the demand side, the global narrative is defined by “structural destruction” within China, formerly the primary engine of global consumption. The anticipated post-pandemic demand boom failed to materialize as economic growth in China decisively decoupled from oil use. This erosion is driven by the rapid saturation of New Energy Vehicles (NEVs) impacting gasoline demand and a massive logistical pivot toward LNG and electric trucks. In 2025, these cleaner alternatives accounted for nearly 50% of new heavy truck sales in China, effectively severing the historical link between industrial activity and diesel consumption—a permanent loss of demand that production cuts cannot reverse.

Looking ahead to 2026, the convergence of these opposing forces points toward a consensus “Super Glut”. Independent agencies like the IEA and EIA project a significant supply surplus exceeding 1.0 mb/d, as non-OPEC growth continues to outstrip global demand. This trajectory suggests a price floor falling toward $55 per barrel, standing in stark contrast to OPEC’s solitary bullish outlook. For economies like Malaysia, this divergence presents a critical risk: relying on optimistic revenue scenarios in a market fundamentally primed for a structural surplus could lead to significant fiscal miscalculations and budget shortfalls.

3. Price Trajectories and the 2026 Outlook

The failure of the OPEC+ strategy has fundamentally reset global price expectations, transitioning the market narrative from a temporary cyclical downturn to a structural bearish consensus. This environment marks the return of the “lower for longer” thesis, as Brent crude is projected to converge toward a $55 floor in 2026—a precipitous decline from the $82 average recorded in 2024. This downward repricing is driven by global inventories reaching four-year highs in late 2025, a data point that effectively erases the historical “scarcity premium” from the price curve. Furthermore, the market now operates under a suppressed upside cap of approximately $75, as participants are acutely aware that OPEC+ retains over 5 mb/d of spare capacity that can be deployed instantly to quash any price rallies. Algorithmic traders have adapted to this structural overhang by treating $55 as a statistical mean-reversion zone and aggressively executing sell orders whenever prices breach the $65 threshold.

While fundamental factors point toward a downward trajectory, geopolitical friction continues to act as a floor defender, creating a sharp bifurcation between crude oil and refined products. Ukraine’s sustained drone campaign against Russian energy infrastructure—evidenced by strikes on major facilities like the Ryazan and Novokuibyshevsk refineries—has removed nearly 20% of Russia’s refining capacity. This has resulted in a unique market paradox: while the global market is awash in excess raw crude, there is a persistent structural tightness in refined products such as diesel and jet fuel. For quantitative analysts, this implies that product margins will remain high even as crude prices soften, as the destruction of refining infrastructure prevents the surplus of raw materials from being converted into usable fuel.

The effectiveness of high-level geopolitical interventions, such as the U.S. “Total Blockade” on Venezuelan oil and the seizure of tankers like The Skipper, has been systematically blunted by logistical market inefficiencies. The rise of “shadow fleets” has rerouted sanctioned cargoes toward Asian hubs, leading to a surge in illicit Ship-to-Ship (STS) transfers off the coast of Malaysia in the East Outer Port Limits. These waters serve as a critical “Malaysian Valve” where sanctioned barrels from Venezuela, Iran, and Russia are blended and re-certified as “Malaysian origin” before being exported to China. By facilitating the continued flow of sanctioned oil, this logistical bypass ensures that the global glut persists, dampening the intended price shocks of Western blockades and maintaining the downward pressure on the 2026 price equilibrium.

4. The Macroeconomic Paradox: Fiscal Squeeze vs. Currency Decoupling

Malaysia confronts a distinct macroeconomic paradox in the 2025–2026 cycle, characterized by a severe revenue squeeze driven by softening oil prices juxtaposed against a surprisingly resilient domestic currency. On the fiscal front, the collapse of the OPEC+ price defense strategy has created a direct budgetary challenge, as the 2025 Federal Budget was premised on Brent crude averaging between $75 and $80 per barrel. The current market reality of approximately $60 per barrel implies a projected revenue shortfall of RM6.8 billion in petroleum income tax (PITA) receipts alone. This fiscal pressure is significantly compounded by what has been termed the “Petronas Dividend Shock,” as the national oil major has lowered its projected 2026 dividend contribution to RM20 billion—a RM12 billion reduction from the RM32 billion contributed in 2025—to preserve capital for mandatory energy transition investments. To mitigate this cumulative RM12 billion revenue gap and maintain national deficit targets, the government has accelerated structural reforms, aggressively replacing lost petro-revenue with fiscal savings generated from targeted RON95 subsidy rationalization and expanded tax collection frameworks such as mandatory e-invoicing.

In a striking defiance of historical patterns, this fiscal deterioration has not triggered the expected currency sell-off, marking the advent of the “Great Decoupling”. Despite benchmark oil prices collapsing from the $80 range to the $60 range, the Malaysian Ringgit (MYR) has appreciated by approximately 7% year-to-date, effectively breaking its decades-long statistical correlation as a “petro-currency”. This resilience is supported by three primary structural shifts: the mandated repatriation of foreign income by Government-Linked Companies (GLCs), narrowing interest rate differentials as the US Federal Reserve enters a cutting cycle while Bank Negara Malaysia maintains a steady policy rate, and a massive influx of Foreign Direct Investment (FDI) into the high-growth Data Center and Semiconductor sectors.

Current quantitative projections for 2026 suggest this decoupling will persist, with the Ringgit expected to stabilize within the 4.10–4.15 range even if oil prices test the $55 floor. However, analysts maintain that a breach of the $50 psychological floor remains a critical tail risk, as such a level could eventually erode the current account surplus to a point where the “Tech Narrative” can no longer fully subsidize the loss of petroleum-linked inflows.

5. Corporate Sector Analysis: Navigating the Downturn

The “Super Glut” environment creates a sharp divergence within the Malaysian Oil & Gas Services and Equipment (OGSE) sector, splitting market participants into two distinct categories: those positioned for volume-driven resilience and those exposed to severe CapEx-driven headwinds. As the custodian of national reserves and the primary shock absorber for the Malaysian economy, Petronas has proactively pivoted toward a “Value over Volume” strategy. Following a 31.7% contraction in FY2024 profits, the national oil company is aggressively ring-fencing cash to meet its RM20 billion dividend commitment and its RM32 billion energy transition (renewables) mandate. This strategic shift necessitates a systematic reduction in generic upstream spending, which fundamentally compresses the available contract pool for domestic service providers.

Within the upstream segment, Hibiscus Petroleum demonstrates high-conviction resilience by utilizing volume expansion as a hedge against price volatility. With the Teal West field scheduled to come online in 2026, the company is targeting a sales growth trajectory toward ~9.2 MMboe, a move designed to offset lower unit realizations. This operational scaling allows the company to maintain its status as a resilient “Cash Cow,” capable of sustaining dividend distributions even if benchmark prices stabilize in the $65 range. Conversely, Velesto Energy exhibits the highest cyclical sensitivity in the current downturn. Data from the Petronas Activity Outlook 2025-2027 confirms a structural decline in Jack-up Rig demand, forecasting a drop from 13 active rigs in 2024 to just 9 by 2027. In a $55/bbl environment, discretionary drilling represents the primary target for budget rationalization, leaving Velesto exposed to a “Utilization Shock” that could compromise both charter rates and interest coverage ratios.

Dialog Group remains the preferred “Safe Haven” for 2026, benefiting from counter-cyclical drivers that thrive in a high-inventory environment. The company is statistically positioned to capture a “Turnaround Boom” in mandatory plant maintenance, which cannot be deferred regardless of oil price action. Furthermore, a global oil glut often triggers a “Contango” market structure—where future prices are higher than spot prices—which increases the demand and pricing power for Dialog’s midstream storage infrastructure. Finally, the report identifies a critical tail risk in the Palm Oil sector via the “Biodiesel Link”. At a $55/bbl crude equilibrium, the discretionary blending of biodiesel becomes economically unviable against cheaper fossil fuels. This loss of a demand floor, combined with the appreciation of the Ringgit which makes exports more expensive for foreign buyers, creates a “Double Bearish” outlook for Crude Palm Oil (CPO) prices heading into 2026.

6. Conclusion: The End of the Supercycle and the “New Malaysian Alpha”

The 2026 outlook marks the definitive end of the post-pandemic commodity supercycle. The data confirms that the “OPEC+ Squeeze” has been structurally neutralized by the dual forces of the “Americas Supply Flood” (US/Brazil efficiency) and “Chinese Demand Destruction” (EV/LNG adoption). We have exited the era of scarcity and entered a period of structural surplus, where $55–$60 per barrel represents not a cyclical bottom, but a new equilibrium anchored by massive spare capacity.

For Malaysia, this transition creates a historic macroeconomic paradox: The Great Decoupling. For the first time in decades, the trajectory of the Ringgit has severed its tether to crude oil. While the fiscal state faces a RM12 billion dividend hole from Petronas—necessitating painful reforms like subsidy rationalization and tax base expansion—the currency itself is thriving on a new diet of Semiconductor exports and Data Center FDI. The “Petro-Currency” label is effectively obsolete; the Ringgit is now a proxy for US Rate spreads and Tech supply chains.

This new reality challenges the historical notion that a “rising tide lifts all boats” within the Oil & Gas sector. Current market dynamics suggest a bifurcation between segments positioned for volume-driven resilience and those exposed to price-driven headwinds.

- High Risk / Headwinds (Cyclical/Price): Pure-play drilling and exploration services (e.g., Velesto Energy) appear most vulnerable to Capex cuts. In a “Value over Volume” environment, discretionary drilling is often the first budget line to be reduced.

- Defensive / Resilient (Volume/OpEx): Infrastructure and Maintenance plays (e.g., Dialog Group) are statistically better positioned to benefit from the physical glut (storage demand) and non-discretionary spending (turnarounds).

- Key Indicator to Watch: The $50 psychological floor. While the Ringgit has decoupled at $60, a crash below $50 remains the primary tail risk. Such a level would erode the Current Account surplus to a point where the “Tech Narrative” can no longer subsidize the loss of “Petro-Dollars.”