The three-decade evolution of Gold (Au), Silver (Ag), Platinum (Pt), and Palladium (Pd) is defined by a complex interplay of macroeconomic forces, shifting monetary policy regimes, and fluctuating industrial demand cycles. This examination deconstructs the pricing behaviors, volatility profiles, and correlation matrices of these assets from 1995 through the record-breaking valuations observed in late 2025.

While the primary lens of the inquiry is global and denominated in United States Dollars (USD), significant emphasis is placed on the Malaysian market. The Malaysian perspective serves as a unique case study in how emerging market currency dynamics—specifically the Malaysian Ringgit (MYR)—interact with global commodity prices to fundamentally alter the risk-return profile for local allocators.

Structural Regimes and Market Cycles

The dataset under review encompasses several distinct market regimes, each offering a rich environment for testing hypotheses regarding safe-haven status and diversification benefits:

- The Disinflationary Era: The bear market of the late 1990s.

- The Commodity Super-Cycle: The expansionary 2000s.

- Post-GFC Expansion: The era of aggressive monetary easing following the 2008 Global Financial Crisis.

- Contemporary Fiscal Dominance: The period of extreme volatility leading into the historic highs of December 2025.

The Malaysian Context and Structural Breaks

From a domestic standpoint, the data is further complicated by idiosyncratic structural breaks. The 1997 Asian Financial Crisis (AFC), the subsequent imposition of capital controls, and the eventual transition to a managed float system necessitate a nuanced approach to volatility modeling.

The interaction between domestic interest rates—represented by the Overnight Policy Rate (OPR) and KLIBOR—and the non-yielding nature of precious metals provides critical insight into the opportunity cost dynamics faced by Malaysian investors. By synthesizing vast arrays of economic indicators and event-driven shocks, this study aims to transcend mere description, offering second and third-order insights into the mechanisms that have driven these markets to their current historic standing.

1. Resilience through Volatility: Global Monetary Cycles and the Malaysian Gold Narrative (1995–2018)

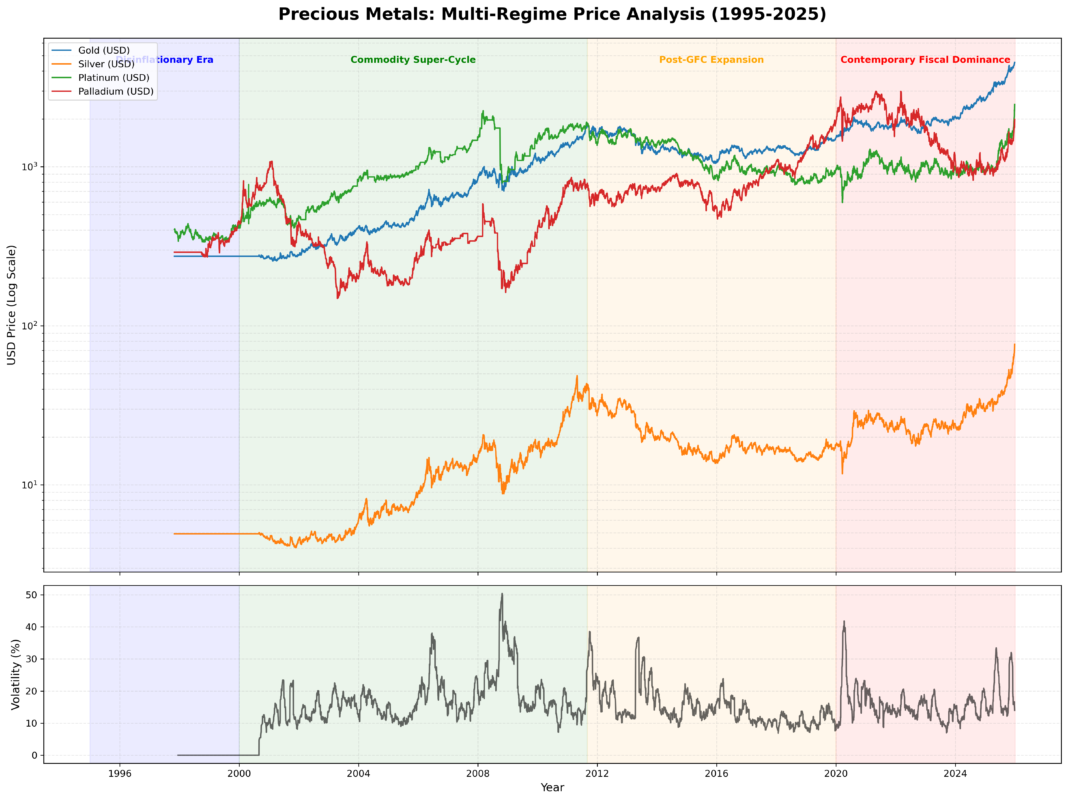

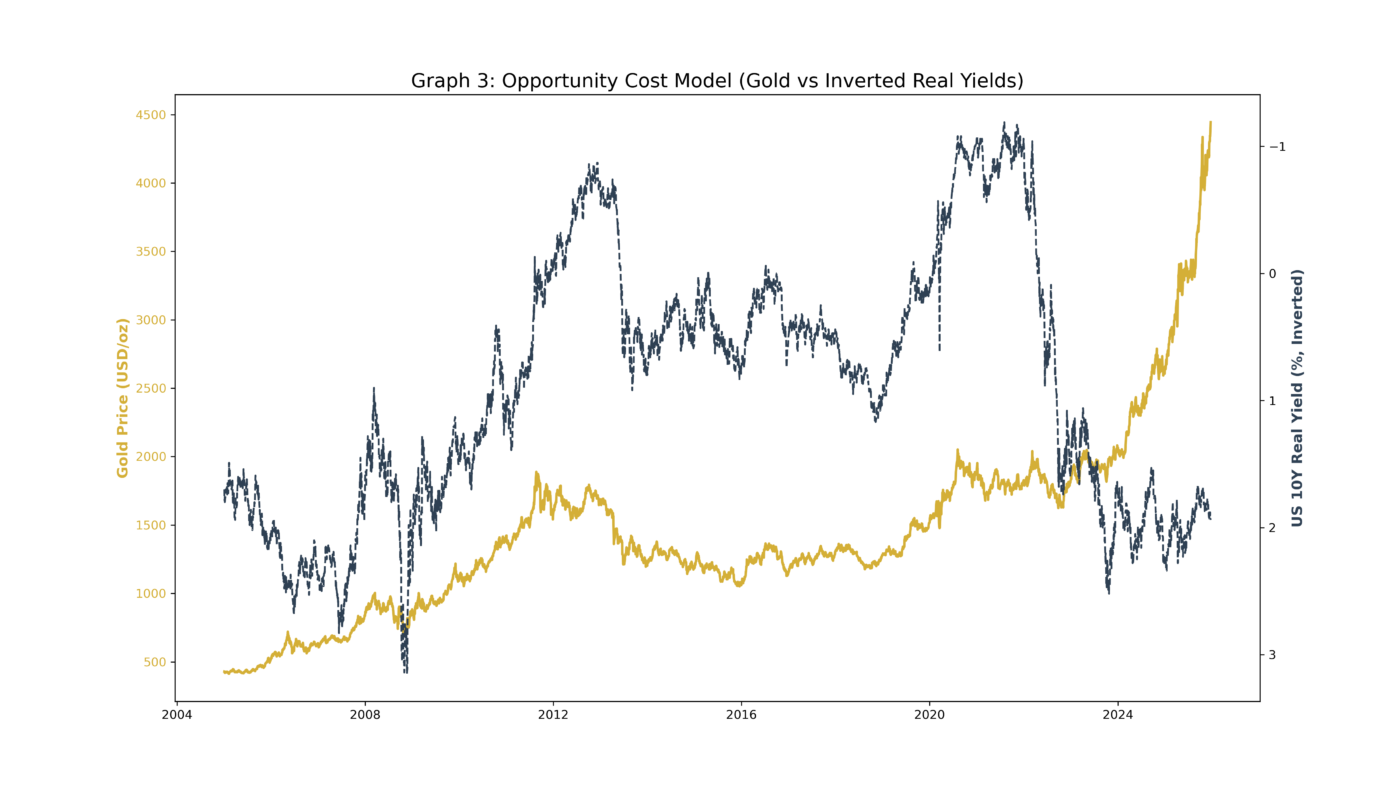

The history of precious metals from 1995 to 2018 is characterized by a transition from a period of global disinflation and central bank divestment to a decade-long secular bull market, followed by a period of stagnation and industrial divergence. During the late 1990s, gold was often dismissed as a “barbarous relic” of a tech-driven economy, struggling to stay above $400/oz as central banks shifted reserves into interest-bearing debt. This trend reversed sharply in the early 2000s, triggered by the bursting of the Dot-com bubble and aggressive monetary easing by the US Federal Reserve. This shift into a period of negative real interest rates and a weakening US dollar initiated a rally that saw gold prices rise by 600%, peaking in 2011. While the 2008 Global Financial Crisis initially caused a 30% drop in gold prices due to liquidity needs and margin calls, the asset eventually decoupled from risk assets and posted positive annual returns as quantitative easing began. However, by 2013, gold entered a brutal bear market after the “Taper Tantrum” caused real yields to soar, leading to a 28% annual drawdown—the largest in three decades.

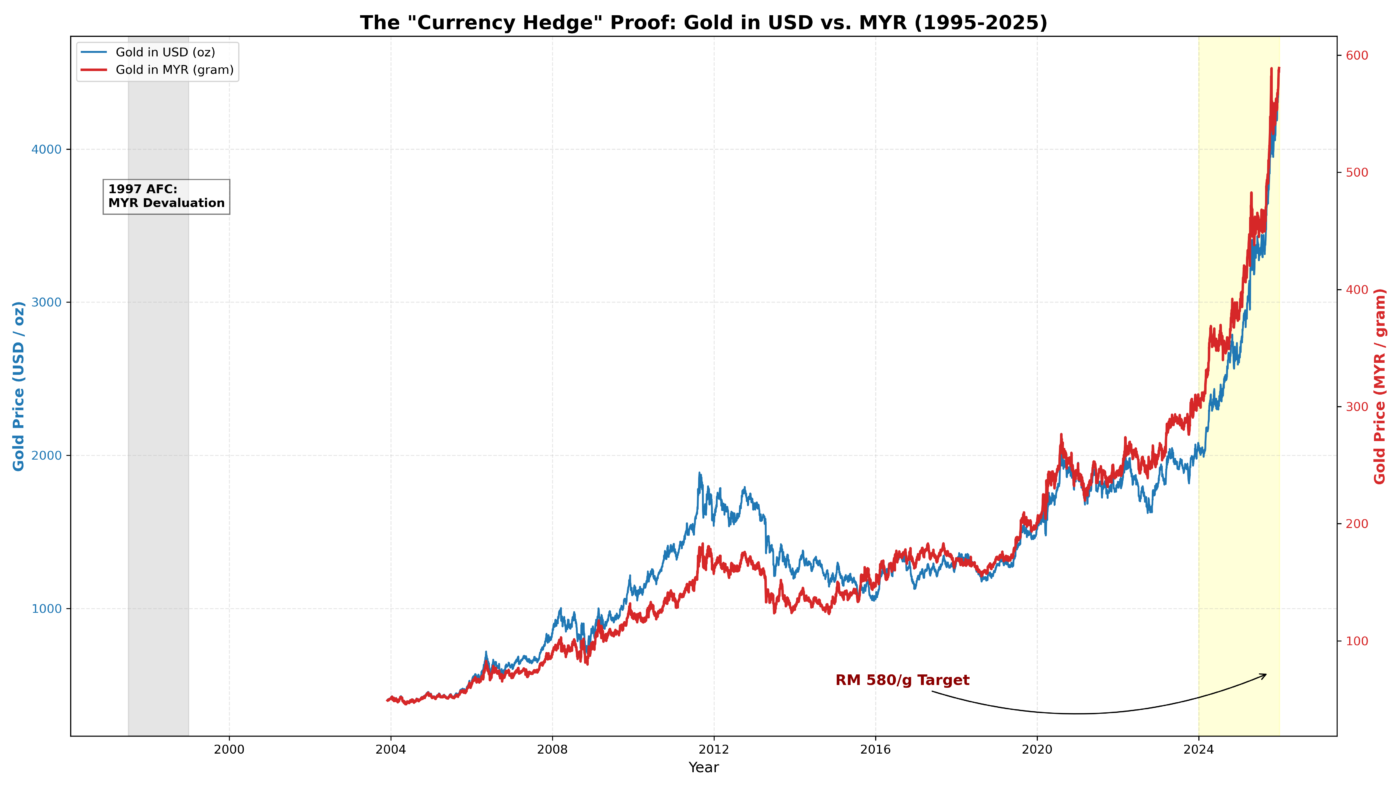

For Malaysian investors, these global cycles were heavily moderated by the volatility of the Ringgit (MYR), which often turned gold into a critical “crisis alpha” currency hedge. During the 1997 Asian Financial Crisis, while gold lost value in USD terms, its nominal MYR value exploded because the Ringgit collapsed from 2.50 to over 4.40 against the dollar. This dynamic shifted between 2005 and 2011; as Malaysia transitioned to a managed float, high oil prices strengthened the Ringgit toward 3.00, which muted the gains local investors saw from the global gold bull market. Later, between 2012 and 2017, domestic political volatility and the 1MDB scandal caused the Ringgit to depreciate once more to over 4.40. This currency weakness provided a vital cushion for local investors, allowing MYR-denominated gold to preserve wealth even as global USD prices remained stagnant.

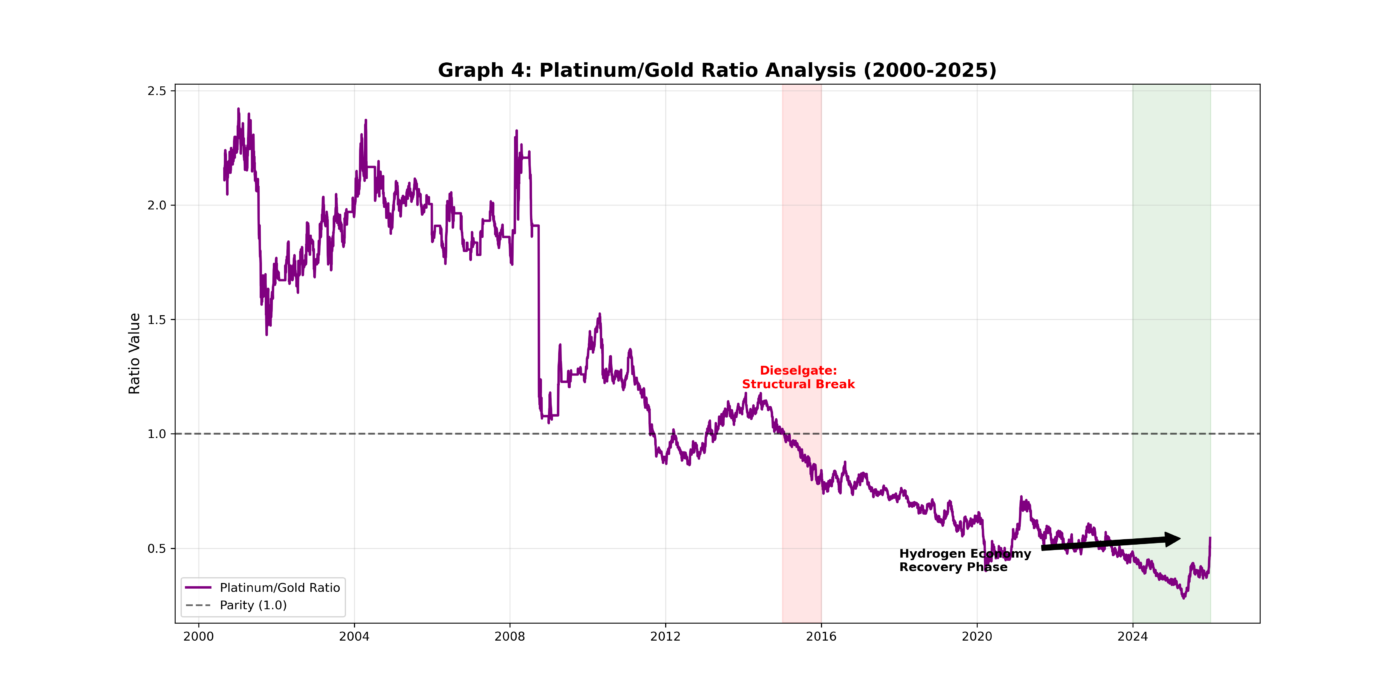

While gold and silver largely followed monetary trends, the Platinum Group Metals (PGMs) demonstrated how industrial cycles can cause permanent structural decoupling. Platinum, which historically traded at a premium to gold, faced an existential crisis following the 2015 “Dieselgate” scandal, where a backlash against diesel engines caused it to flip to a massive, persistent discount against gold. In contrast, palladium entered a structural bull market as the automotive industry shifted toward gasoline engines, which utilize palladium for emissions control. Driven by supply disruptions in Russia and chronic underinvestment, palladium prices doubled between 2016 and 2019, illustrating that supply constraints and low industrial substitutability can drive explosive growth regardless of broader market stagnation.

2. The Pandemic, Inflation, and Financial Repression (2019–2025)

The period between late 2019 and 2025 has been defined by extreme monetary elasticity, beginning with the 2019 repo market turmoil and escalating through the COVID-19 pandemic. During the initial pandemic panic of March 2020, a systemic “dash for cash” caused asset correlations to converge, leading to sharp temporary drawdowns where gold fell 12% and silver collapsed by over 30%. However, this solvency crisis was short-lived as central banks, led by the Federal Reserve, implemented “unlimited QE” that pushed real yields below -1.0%, sparking a V-shaped recovery in precious metals. In Malaysia, Bank Negara supported this trend by slashing the Overnight Policy Rate (OPR) to a record low of 1.75%, which reduced the opportunity cost of gold and spurred retail interest in Gold Investment Accounts (GIAs).

By late 2025, the market transitioned into a historic “melt-up” as precious metals evolved from safe havens into primary macro hedges against sovereign debt instability. This repricing saw gold deliver a 70% annual return, breaching the $4,500/oz mark, while silver surged by 150% to end the year near $74/oz due to acute industrial deficits. This synchronized explosion across the metals complex reflects a growing market consensus that global sovereign debt levels have become unsustainable without further currency debasement.

Platinum Group Metals (PGMs) also experienced a dramatic structural shift during this period. Platinum staged a massive recovery of approximately 150%, reaching over $2,300/oz, fueled by supply failures in South Africa and the asset’s critical role in the emerging hydrogen economy. Similarly, palladium rose 90% as automakers struggled with low substitutability and tightening environmental regulations. These moves underscore how structural supply-demand imbalances can lead to violent price decoupling when they intersect with a broader monetary bull market.

For the Malaysian economy, the 2025 rally has transformed gold into a vital “household financial shield”. With local prices exceeding RM 580/g, gold has effectively strengthened household balance sheets without increasing consumer debt. In an environment marked by a rising cost of living, these traditional gold savings have provided an essential liquidity buffer and served as a “quiet stabilizer” for families, preserving purchasing power against both domestic and global inflationary pressures.

3. Strategic Outlook: The Malaysian Market and the 2026 Horizon

The strategic landscape for Malaysian investors in late 2025 is defined by a non-linear relationship betThe strategic landscape for Malaysian investors in late 2025 is defined by a non-linear relationship between domestic interest rates and precious metal valuations. While the Overnight Policy Rate (OPR) currently stands at 2.75%—an increase from the pandemic-era lows of 1.75%—the real yield remains deeply negative. With 2025 headline inflation averaging 5.2% and core asset appreciation rates exceeding double digits, the effective real interest rate of -2.45% continues to drive institutional capital away from cash and into precious metals.

This environment continues to catalyze a “flight to real assets.” For a MYR-denominated portfolio, gold provides a unique triple-advantage: it serves as a correlation breaker against KLCI volatility, an FX overlay that mimics USD-denominated assets without foreign account requirements, and a tax-efficient vehicle largely exempt from Sales and Service Tax (SST).

Looking ahead to 2026, quantitative data suggests the structural bull market will persist, albeit with heightened volatility as the market enters a “price discovery” phase at historic highs. Current institutional consensus models have been revised upward to reflect this shift:

- Global Target Aggregates: Projections indicate gold reaching $5,000/oz by Q4 2026, supported by massive central bank accumulation averaging 585 tonnes per quarter.

- Central Bank Diversification: Quantitative models forecast continued diversification of reserves, with monthly purchases expected to average 70 tonnes.

- Consensus Price Models: Market estimates place the average gold price at $4,550/oz for the year, indicating the cycle is advanced but fundamentally supported.

Industrial metals are expected to maintain a higher Beta than gold as structural deficits intensify. Silver is projected to consolidate its 2025 gains before targeting $85–$90/oz in late 2026. This trajectory is supported by a further contraction in the Gold/Silver ratio toward historical mean levels and a structural supply deficit as industrial demand in the solar and electronics sectors reaches a multi-decade peak. Similarly, industry supply-demand data for Platinum Group Metals (PGMs) expects deficits to persist, with platinum targets increasing significantly due to the potential easing of internal combustion engine (ICE) bans in specific global jurisdictions.

For the local investor, the 2026 outlook remains sensitive to the USD/MYR exchange rate. While the Ringgit has strengthened to approximately 4.13 in late 2025, any future USD resurgence would provide a “double-kick” to local gold prices. Domestic institutional sentiment remains robustly bullish, maintaining a positive trading bias with resistance targets aligned with global benchmarks, viewing precious metals as a critical hedge against falling real yields.

4. Conclusion: The Paradigm of Commodity Monetization

The movement of precious metals over the past 30 years describes a trajectory from irrelevance to indispensability. The quantitative data unequivocally demonstrates that Gold is not merely a commodity but a monetary asset. The historic performance of 2025, where all four metals posted double-to-triple digit gains, marks a potential paradigm shift—a “commodity monetization” event where tangible assets are aggressively repriced against fiat currencies.

For the Malaysian investor, the data suggests that precious metals are no longer optional “insurance” but mandatory portfolio components. The ability of these assets to capture “Crisis Alpha” during regional shocks, combined with their role as a hedge against Ringgit depreciation, remains their most potent quantitative characteristic. As the global market marches toward the $5,000 gold milestone in 2026, the interplay between Malaysia’s managed float, domestic OPR levels, and industrial “green inflation” will define the next cycle of wealth preservation.