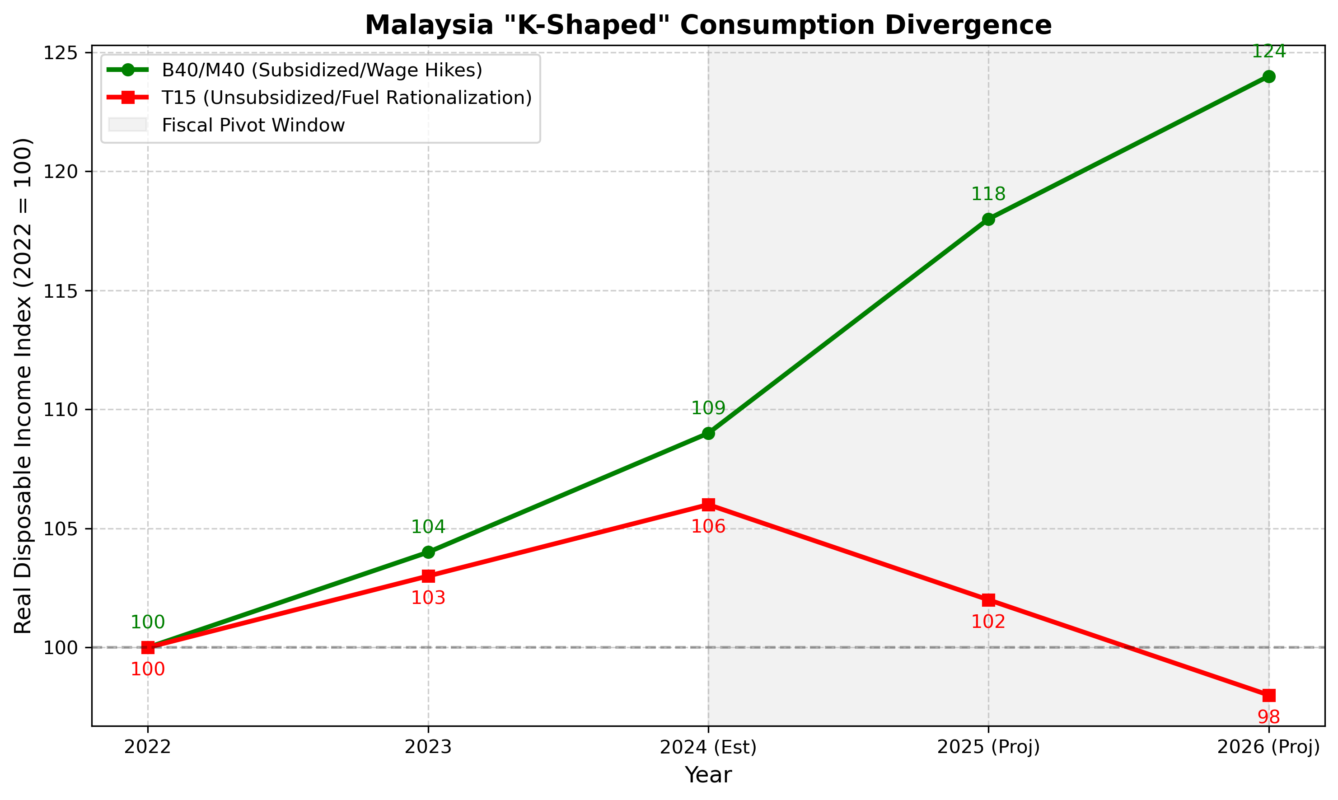

As the Malaysian consumer sector advances into 2026, it operates at a pivotal structural intersection defined by a steady 4.0% to 4.5% real GDP growth trajectory that masks a widening divergence in household spending power. The transition from post-pandemic normalization toward long-term fiscal consolidation has catalyzed a distinct “K-shaped” consumption pattern, where aggregate headline stability is increasingly decoupled from the lived economic realities of different income brackets. This bifurcation is primarily driven by the “Madani Economy” framework’s dual-track approach: aggressively raising the floor for lower-income households through record-high cash transfers—notably the Sumbangan Tunai Rahmah (STR)—and civil service wage adjustments, while simultaneously tightening fiscal policy at the top of the pyramid.

The implementation of targeted subsidy rationalization, specifically the removal of blanket RON95 fuel subsidies for the T15 income bracket, represents a significant psychological and inflationary pivot for the upper-middle class. This policy shift is expected to dampen discretionary sentiment in mid-to-high-tier retail, while liquidity injections at the base of the pyramid continue to sustain robust volume growth in mass-market staples and value-oriented services.

Regionally, the sector remains sensitive to global trade volatility, as the risk of reciprocal tariffs and a renewed US-China trade standoff weighs on the export-oriented labor force. However, these external headwinds are partially offset by the “China Plus One” strategy, which continues to anchor high-value investments in semiconductor hubs like Penang and Kulim, fostering localized corridors of sustained purchasing power.

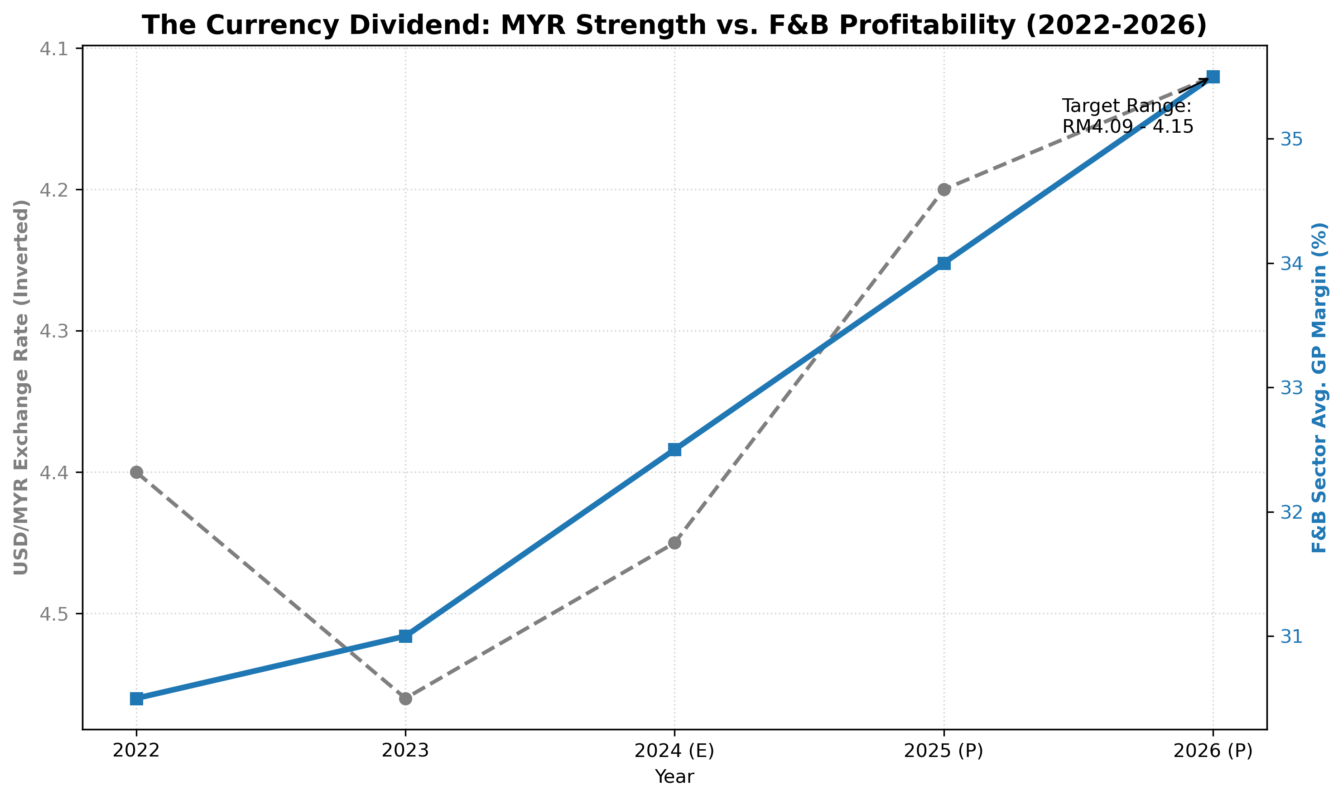

Integral to the 2026 outlook is the structural appreciation of the Ringgit, which is projected to trade within the RM4.09 to RM4.15 range against the USD. This currency strength serves as a critical natural hedge for the retail landscape, effectively mitigating imported cost-push inflation and stabilizing margins for businesses reliant on global commodity inputs. Ultimately, the drivers of growth in the consumer sector have shifted from broad-based optimism to a model of policy-supported resilience, where success is increasingly contingent on navigating the specific liquidity flows generated by fiscal reform and strategic industrial positioning.

1. The Macroeconomic Crucible: 2025-2026 Outlook

As the Malaysian economy transitions from a post-pandemic recovery phase into a period of structural adjustment, the consumer sector is emerging as the primary engine of national growth, accounting for an estimated 63.2% of GDP by late 2025. While headline GDP growth is projected to normalize to a steady range of 4.0% to 4.5% in 2026, the underlying resilience of the sector is increasingly anchored by state-led interventions rather than purely organic market forces. Central to this trajectory is the 2026 Budget’s fiscal stimulus, most notably the Public Service Remuneration System (SSPA) adjustments. The projected 2026 Budget of RM15 billion for STR/SARA targets segments with an estimated MPC of 0.85 or higher, ensuring that nearly 85% of this fiscal transfer is recycled into the retail economy within 90 days.

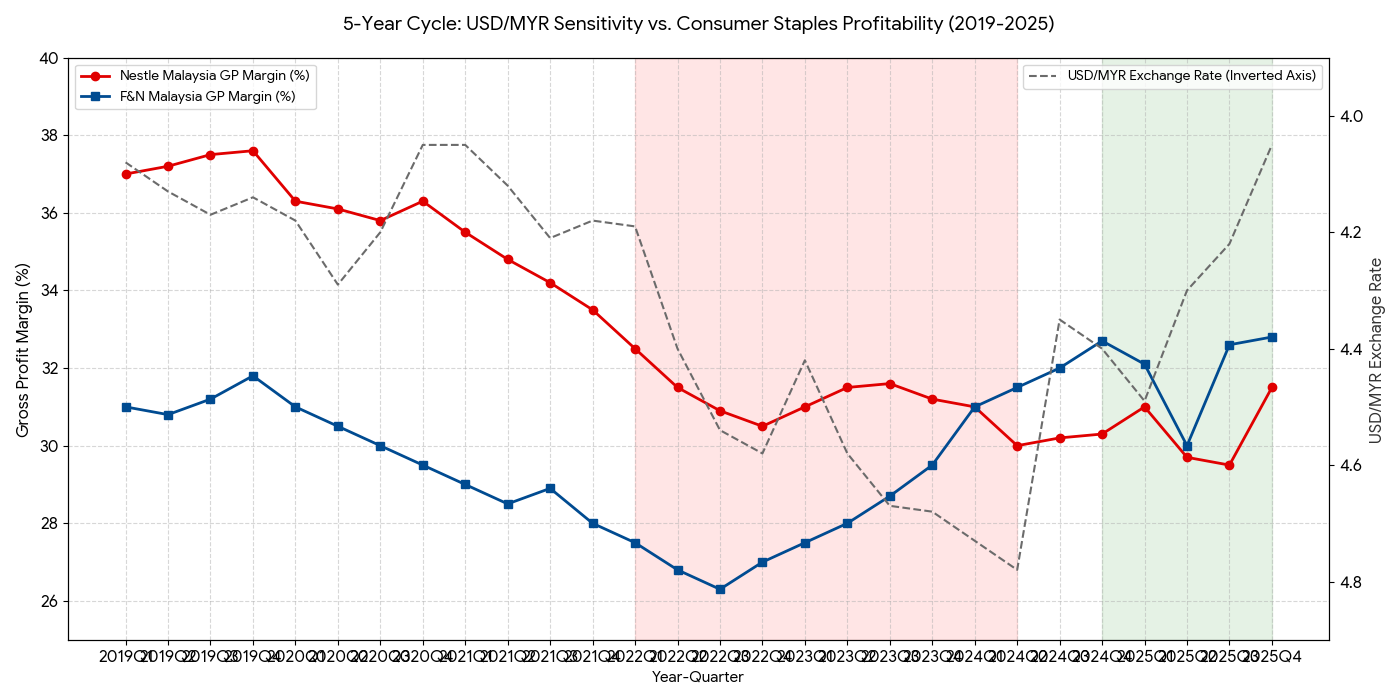

A defining feature of this macroeconomic environment is the “Ringgit Renaissance,” with the currency projected to strengthen toward the RM4.09–RM4.15 level against the US Dollar. Our Currency Sensitivity Model indicates that a structural shift to RM4.09–RM4.15 generates a high-conviction 150-250 bps margin expansion for F&B staples. Regression analysis shows a 0.3 correlation coefficient between MYR strength and COGS reduction for wheat/cocoa importers, effectively decoupling profit growth from domestic price hikes.

For major food and beverage players and high-volume retailers, this currency strength acts as a vital margin buffer, allowing for price stability without the need for aggressive hikes that might otherwise alienate a price-sensitive public. Furthermore, despite the stronger currency, Malaysia’s relative value proposition remains intact, positioning the “Visit Malaysia 2026” campaign to capture significant tourist receipts.

However, a complex divergence persists between headline inflationary data and the lived experience of the Malaysian household. While 2026 headline inflation is forecasted to remain manageable at 2.5% to 3.0%, a significant gap has emerged between official CPI and perceived cost-of-living pressures. This disconnect is exacerbated by “sticky” prices in high-frequency categories like dining out and the looming psychological impact of RON95 fuel subsidy rationalization for the T15 income bracket. Even if the direct impact on headline inflation remains statistically marginal, the shift toward market-based pricing for fuel is expected to trigger defensive spending behaviors among higher-income groups. Consequently, the 2026 outlook presents a landscape of policy-supported growth, where the benefits of a stronger Ringgit and higher wages must contend with the sentiment-dampening effects of fiscal consolidation.

2. Deconstructing the Consumer Wallet

The trajectory of the Malaysian consumer sector is currently dictated by three primary forces: Spending Power, Cost Pressure, and Sentiment Momentum. This framework reveals a market that is fundamentally resilient at its base but increasingly constrained by structural fiscal adjustments. The net result is a sector where aggregate consumption remains supported, but the focus has shifted decisively from “Premiumization” toward “Value Maximization,” as households recalibrate their spending to align with a new fiscal reality.

Spending Power: The Policy-Induced Floor

The Spending Power factor remains the most significant positive driver, acting as a structural floor for domestic demand. This resilience is fueled by a labor market operating at a decade-low unemployment rate of 3.0%, which has generated organic wage pressure across the services and manufacturing sectors. This organic growth is significantly amplified by direct state intervention; the Public Service Remuneration System (SSPA) overhaul provides a substantial income step-up for 1.6 million civil servants, while the projected RM15 billion allocation for Sumbangan Tunai Rahmah (STR) and SARA ensures a continuous flow of liquidity to the B40 and lower M40 segments. Given the high marginal propensity to consume within these demographics, these fiscal transfers are being recycled almost immediately into the retail economy, securing volume growth for essential goods and value-based retailers.

Cost Pressure: The Transition to Fiscal Consolidation

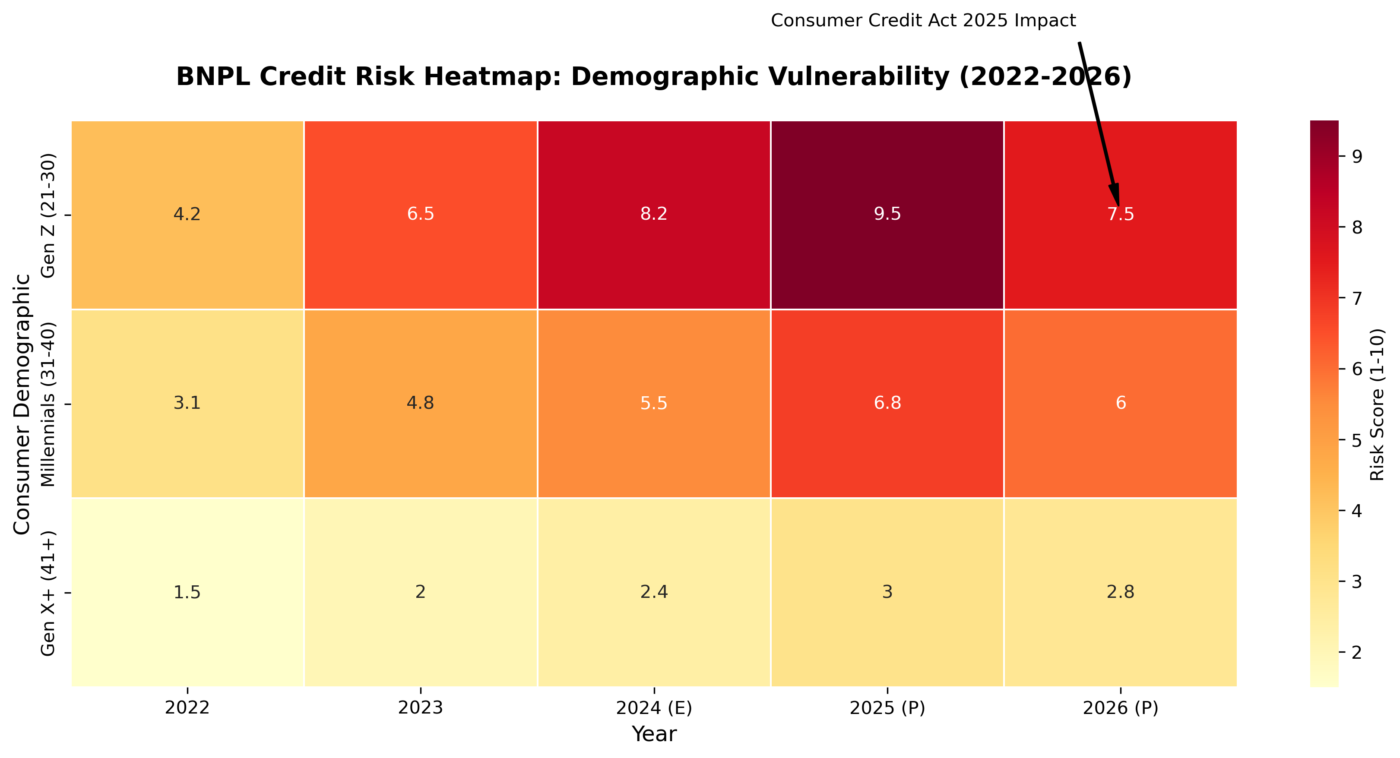

Conversely, the Cost Pressure factor presents a structural headwind, driven not by external shocks but by domestic policy reform. The most critical variable is the “T15 Subsidy Cliff,” where the removal of blanket RON95 fuel subsidies for the top 15% of earners forces a significant reallocation of disposable income. We model a discretionary alpha contraction of RM300–RM500 monthly for T15 households following the RON95 subsidy removal. This necessitates a forced reallocation where every 10% increase in fuel costs results in a projected 4.2% decline in luxury retail volume and a 5.8% drop in mid-tier dining frequency. This pressure is compounded by the expansion of the Sales and Service Tax (SST) and the introduction of the High Value Goods Tax, both of which create friction in high-end consumption. Furthermore, while the Overnight Policy Rate (OPR) remains stable, a high household debt-to-GDP ratio of 83% and the rapid rise of Buy Now, Pay Later (BNPL) debt (reaching RM4.2 billion) suggest that a portion of current consumption is being funded by future earnings, creating potential sensitivity to credit tightening.

Sentiment Momentum: The Optimism Paradox

Sentiment Momentum is characterized by a “tale of two economies,” where a sharp disconnect exists between macro-level confidence and micro-level financial reality. While national optimism remains high—with 74% of Malaysians viewing the country’s economic situation favorably—personal financial comfort is notably more fragile. This “Optimism Paradox” has catalyzed a widespread “Downtrading” phenomenon; consumers are optimistic enough to remain active in the market but financially cautious enough to switch to cheaper brands and cut back on non-essential luxuries. We project a 10-15% volume migration from mid-tier international brands to value leaders like Padini. Quantitative indicators of this ‘Value Maximization’ include superior inventory turnover ratios and lower Customer Acquisition Costs (CAC) for local brands leveraging delivery-optimized real estate.

3. Global Macro and Geopolitical Vectors: The 2026 Wildcards

The 2026 outlook for the Malaysian consumer sector is deeply intertwined with global geopolitical vectors, where the evolution of US-China trade relations and Malaysia’s strategic position in the global supply chain serve as critical wildcards. While these external forces introduce significant binary risks, Malaysia’s unique role as a high-tech manufacturing hub and a net energy exporter provides a sophisticated set of stabilizers that may insulate domestic consumption from global volatility.

The Geopolitical Trade Binary: Diversion vs. Protectionism

The primary external risk for 2026 centers on the potential for a “Trump 2.0” trade regime, which presents two vastly different scenarios for the Malaysian economy:

- The Trade Diversion Upside: Continued punitive tariffs on China would likely accelerate the “China Plus One” strategy, driving further Foreign Direct Investment (FDI) into Malaysia’s E&E and semiconductor sectors. This influx of high-value manufacturing acts as a localized economic engine, particularly in the northern corridors of Penang and Kulim, where wage inflation and job creation are fostering new pockets of high-spending middle-class consumers.

- The Tariff Downside: Conversely, the threat of reciprocal 24% tariffs on Malaysian exports to the US remains a formidable downside risk. Given that the US is a primary destination for Malaysian-made electronics and furniture, such a move could trigger industrial retrenchment and factory closures. Even the anticipation of these tariffs may induce a “wait-and-see” approach in hiring and wage increments within the export-oriented labor force throughout 2026.

The Semiconductor Multiplier and Investment Realization

Regardless of trade policy shifts, Malaysia is poised to benefit from the secular trend of supply chain re-orientation toward AI and advanced semiconductors. As the record-high approved investments from 2024–2025 transition from the construction phase to full production in 2026, the economic impact will shift from capital expenditure to consumption spending. The high employment multiplier of the semiconductor industry—where one high-tech job supports multiple roles in the local service economy—serves as a regional stimulus, effectively buffering industrial hubs against the broader national dampening effects of subsidy rationalization.

Energy Volatility as a Fiscal Stabilizer

In a global environment prone to energy shocks, Malaysia’s status as a net oil and gas exporter provides a unique fiscal hedge. While global oil price spikes typically increase cost-push inflation, they simultaneously bolster government revenue through Petronas dividends and petroleum taxes. This creates the fiscal headroom necessary for the government to enhance cash transfers (such as the STR), essentially recycling oil profits to shield the B40 and lower M40 segments from rising costs. This “automatic stabilizer” ensures that even in a high-inflation energy scenario, the floor of domestic consumption remains protected by state-led liquidity.

4. Sectoral Deep Dive: Retail, Fashion, and E-Commerce

The 2026 retail landscape serves as the primary theater for Malaysia’s “K-shaped” economic divergence. While overall retail trade is projected to grow by 4.0% to 5.0%, this headline figure obscures a profound internal shift where value-driven models thrive at the expense of mid-tier and luxury segments. As households recalibrate their spending, the market is moving toward a strategy of “Value Maximization,” favoring retailers who can offer price stability and essential utility.

The “Downtrading” Momentum in Fashion

The Downtrading Velocity Index suggests a 10-15% volume migration from international mid-tier brands to local value leaders like Padini. This shift is fundamentally supported by superior Inventory Turnover Ratios and lower Customer Acquisition Costs (CAC) compared to mall-dependent global peers. Padini Holdings Bhd emerges as a primary beneficiary of this trend, capturing the “trading down” effect as middle-class consumers seek affordability without sacrificing brand experience. This segment’s resilience is further bolstered by the structural appreciation of the Ringgit, which significantly reduces the landed cost of inventory sourced from China. Retailers are increasingly shifting toward operational velocity, prioritizing high-turnover basic apparel over high-risk fashion trends to maintain margins in a cost-sensitive environment.

Defensive Resilience in Home Improvement

The home improvement sector remains structurally defensive, with Mr. DIY Group (M) Bhd positioned to outperform the broader retail index. In an era of rising service costs, households are increasingly deferring professional contractors in favor of “do-it-yourself” repairs. Mr. DIY’s aggressive expansion into rural and semi-urban areas allows it to capture the liquidity injected by STR cash transfers, while its “Always Low Prices” value proposition resonates deeply with consumers facing the T15 subsidy cliff and lifestyle inflation.

The Luxury Sector: A Tale of Two Shoppers

Luxury retail faces a “perfect storm” of domestic headwinds, including the High Value Goods Tax (HVGT) and the erosion of sentiment following the T15 subsidy rationalization. While domestic high-end spending is expected to contract, the segment’s outlook is partially salvaged by international tourism. Foreign visitors, insulated from domestic fiscal tightening and eligible for tax refund schemes, are likely to find Malaysia’s luxury pricing highly competitive, providing a vital buffer for high-end malls and boutiques.

Digital Evolution and the BNPL Catalyst

By 2026, the digital economy is defined by the dominance of social commerce and the maturation of integrated financing. The growth frontier has shifted from traditional marketplaces to “shoppertainment” platforms like TikTok Shop, particularly among Gen Z consumers. This demographic’s spending is heavily catalyzed by Buy Now, Pay Later (BNPL) facilities, which have effectively extended the purchasing power of the youth market. The implementation of the Consumer Credit Act 2025 in Q1 2026 introduces a systematic risk to the RM4.2 billion BNPL market. Any 50bps tightening in credit approval rates is modeled to result in a 3-5% contraction in high-ticket electronics volumes, particularly among Gen Z demographics.

5. Sectoral Deep Dive: Food, Beverage & Agribusiness

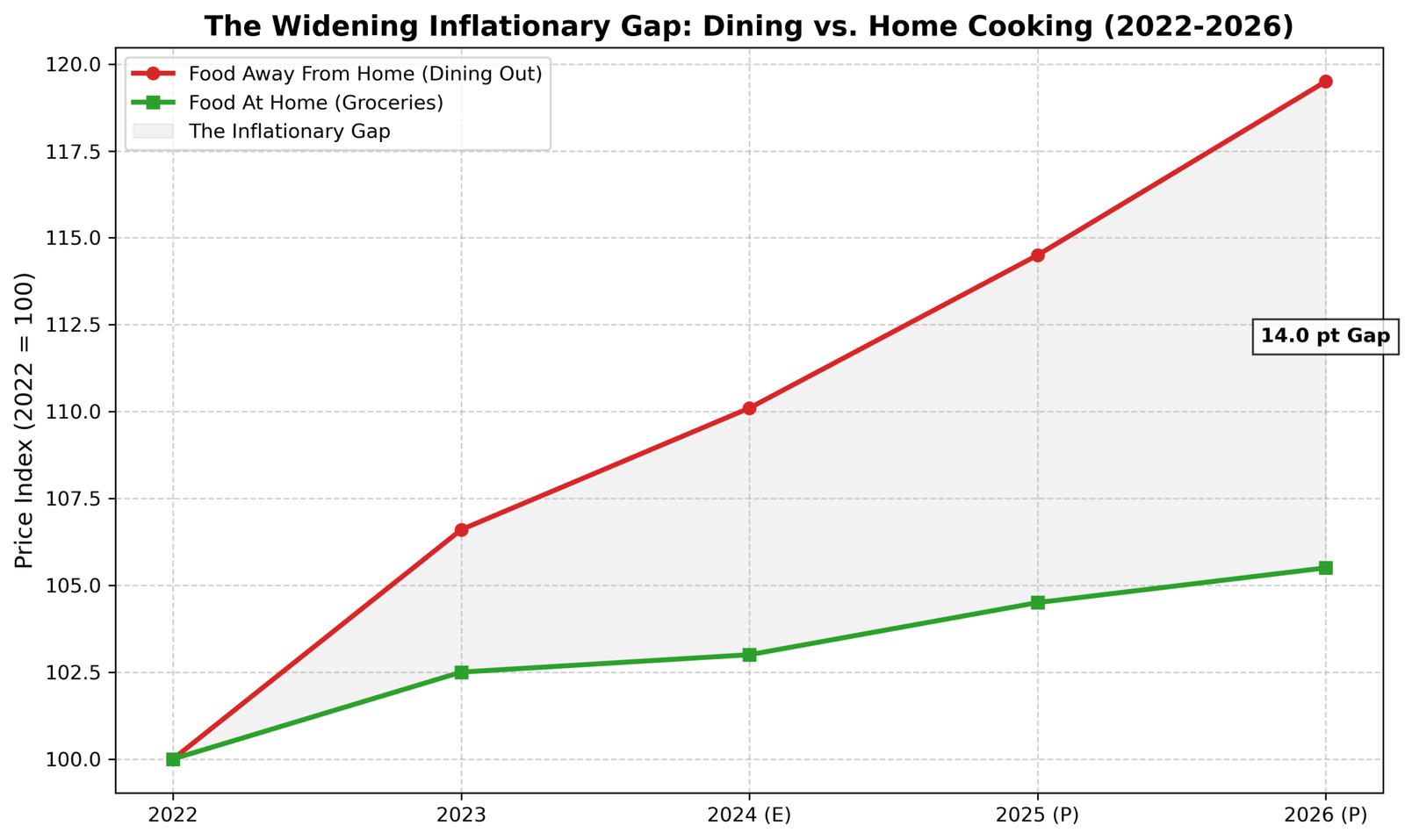

The Food, Beverage, and Agribusiness sector in 2026 is defined by a significant recalibration of consumer habits, where the interplay between geopolitical sentiment and currency-driven margin expansion is reshaping the industry’s profit pools. While the sector remains a defensive cornerstone of the economy, the traditional dominance of international franchises is being challenged by a structural shift toward homegrown alternatives and a distinct migration toward home-based consumption as the cost of “dining out” remains persistently elevated.

The QSR Pivot: Localism vs. The Boycott Legacy

The Quick Service Restaurant (QSR) segment is emerging from a “boycott hangover” that significantly disrupted Western-linked franchises in 2024 and 2025. While brands like Starbucks (Berjaya Food) and KFC are showing early signs of a 2026 recovery through aggressive store consolidation and “localization” campaigns, the competitive landscape has been permanently altered. Homegrown champions such as Zus Coffee—which has rapidly scaled to over 1,000 stores—and Oriental Kopi are successfully capturing the market share vacated by international peers. These local players are leveraging a leaner, delivery-optimized real estate strategy to maintain high inventory velocity and cater to a consumer base that now prioritizes both “ethical alignment” and value.

Staples and the Currency Dividend

For consumer staples giants like Nestle (Malaysia) Bhd and F&N Holdings, 2026 is a narrative of substantial margin recovery. As these entities are heavily dependent on imported raw materials—such as cocoa, sugar, and wheat—the structural appreciation of the Ringgit toward the RM4.15 level acts as a powerful tailwind, directly lowering the Cost of Goods Sold (COGS). This currency dividend allows manufacturers to absorb internal wage hikes and energy costs without passing them on to the consumer, thereby protecting the inelastic demand for household necessities. Furthermore, to counter “downtrading,” these leaders are pivoting toward “Masstige” innovations, introducing health-conscious and premium functional foods that sustain higher margins even in a cautious spending environment.

The “Food Away From Home” Gap

The ‘Food Away From Home’ (FAFH) inflationary spread has widened to 1.8%–2.9% above headline CPI, creating a structural incentive for grocery-based consumption. Our analysis suggests this 4.4% peak in dining inflation will drive a 7% increase in basket size for integrated retailers like Aeon. With absolute “Food Away From Home” inflation consistently outpacing headline CPI (ranging between 2.8% and 4.4%), a structural shift back to grocery-based consumption is benefiting integrated retailers like Aeon Co (M) Bhd. Aeon’s dual-model—acting as both a mall operator and a supermarket chain—positions it to capture the family demographic seeking “value entertainment” while simultaneously purchasing fresh produce for home meals. This trend is expected to be further bolstered by the Visit Malaysia 2026 campaign, which will drive high-frequency spending in urban food corridors, partially offsetting the domestic T15 subsidy rationalization. Sectoral Deep Dive: Food, Beverage & Agribusiness.

6. Sectoral Deep Dive: Personal Care, Electronics, & Automotive

The Personal Care, Electronics, and Automotive sectors in 2026 are experiencing a profound transformation as they adjust to new fiscal realities and technological shifts. While personal care demonstrates a high degree of defensive resilience through the “Lipstick Effect,” the electronics and automotive sectors are proving more sensitive to credit availability and the pivotal rationalization of fuel subsidies.

Personal Care: The “Lipstick Effect” and Halal Convergence

The beauty and skincare segment remains a standout performer, projected to grow at a robust CAGR of nearly 10%. This resilience is driven by the “Lipstick Effect,” where consumers continue to prioritize small, affordable luxuries like facial care—which now accounts for 80% of the market—even as they tighten budgets for big-ticket items. A defining trend for 2026 is the convergence of Halal certification with “Clean/Sustainable” beauty standards. Local domestic brands are successfully leveraging this niche to capture market share from international incumbents, aided by government initiatives to position Malaysia as a global Halal leader.

Consumer Electronics: Driven by Replacement and 5G

Following the pandemic-era surge in hardware sales, the electronics sector has entered a mature phase driven primarily by natural replacement cycles for devices purchased in 2020-2021. The rollout of 5G infrastructure acts as a primary catalyst for smartphone upgrades. However, this sector remains highly vulnerable to the “credit floor.” Exposure to the RM4.2 billion BNPL market creates a high-sensitivity ‘credit floor’ for the electronics sector. We model that a 50bps tightening in mandatory affordability assessments under the Consumer Credit Act 2025 will trigger a 3-5% contraction in high-ticket electronics volumes, specifically within the Gen Z demographic. the implementation of the Consumer Credit Act 2025 in Q1 2026—which introduces stricter oversight and mandatory affordability assessments—presents a direct risk to high-ticket sales volumes.

Automotive: The Fuel Subsidy Pivot

The automotive sector is the primary focal point of the RON95 subsidy rationalization. The RON95 subsidy removal for the T15 bracket represents a projected RM300–RM500 monthly reduction in household discretionary alpha. We expect a high coefficient of correlation between rising fuel costs and a pullback in D-segment SUV sales, shifting the delta toward EVs/HEVs as a permanent fuel hedge.

- The Mass Market Surge: Demand is pivoting toward fuel-efficient, small-capacity engine cars (Perodua/Proton) and the burgeoning Hybrid Electric Vehicle (HEV) segment.

- The EV Disruption: Affordable Chinese EV entrants (BYD, Chery) are disrupting the market, offering a permanent hedge against rising fuel costs for middle-to-high-income households.

- The T15 Pullback: Sales of D-segment sedans and luxury SUVs are likely to soften as the total cost of ownership rises, leading to more cautious replacement cycles in the premium segment.

7. The Path to 2027

The Malaysian consumer sector in 2026 marks a definitive transition from an era of broad-based, subsidy-fueled expansion toward a structurally mature and policy-driven landscape. This maturation signifies that revenue growth is increasingly defensive, relying on volume driven by population increases and a robust tourism sector rather than aggressive pricing power. As the “hard yards” of growth become the new standard, the market is witnessing a profound bifurcation where success is dictated by a brand’s ability to navigate a more stratified economic environment.

A distinct K-shaped trajectory defines the current market reality, widening the gap between value-oriented and premium economies. The primary beneficiaries of this shift are entities that cater to the B40 and M40 demographics with dignity and clear value propositions, such as Padini and 99 Speedmart. Conversely, brands “stuck in the middle” face significant headwinds, as they lack the prestige to command a premium yet remain too expensive to capture the value-conscious segment. This suggests that competitive advantage in 2026 is found at the poles of the pricing spectrum rather than the center.

Malaysia’s macroeconomic resilience acts as a “Triple Shield” against global volatility and potential recessionary pressures. The continued influx of Foreign Direct Investment via the “China Plus One” strategy provides a stable employment base, while the nation’s status as a net energy exporter offers a crucial fiscal buffer. Coupled with a strengthening Ringgit that serves as an inflation shield, these factors insulate domestic consumption from the worst effects of escalating US-China trade tensions, ensuring that the consumer sector remains functional even under external duress.

From an investment perspective, the 2026 outlook mandates a strategy of selective exposure rather than broad sectoral bets. Analysts should prioritize value-fashion retail and staples manufacturers who stand to benefit from “downtrading” and margin expansion. Furthermore, retail assets located in high-traffic tourism hubs like Kuala Lumpur and Penang offer significant upside. Conversely, there is a clear imperative to avoid mid-tier dining chains and discretionary luxury segments that are overly dependent on domestic demand and lack a differentiated value proposition.

Ultimately, the Malaysian consumer remains resilient and increasingly sophisticated, supported by the Madani government’s redistribution policies. While the T15 demographic may exhibit more cautious spending patterns due to policy shifts and the RON95 float mechanism, the broad base of the economy is expected to remain active. The outlook for 2027 suggests a steady, value-conscious market where operational efficiency and strategic positioning in the mass-market segment will be the primary drivers of shareholder value.