As of late December 2025, the Malaysian plantation sector has reached a historic inflection point. This past year was defined by a fundamental transition, moving away from post-pandemic recovery and into a new era characterized by rigorous regulatory compliance and high-value diversification. Amidst these shifts, the national economy proved its resilience; Gross Domestic Product (GDP) is projected to grow between 4.5% and 5.5% for the year, bolstered by an agricultural sector that consistently exceeded growth expectations.

The industry navigated 2025 with a blend of mixed fortunes and overall stability. Defying earlier bearish forecasts, Crude Palm Oil (CPO) prices remained robust, closing the year firmly above the critical RM4,000 per tonne psychological threshold. Meanwhile, the “Durian Gold Rush” matured from a speculative narrative into a tangible export powerhouse, following the successful completion of the first full year of fresh fruit access to the Chinese market.

As the sector braces for the immediate enforcement of the European Union Deforestation Regulation (EUDR) on 30 December 2025, the industry has rapidly accelerated its digitization and traceability efforts across the entire supply chain. This strategic briefing synthesizes the latest FY2025 corporate financial results, commodity price dynamics, and trade statistics to present a data-driven investment thesis for the year ahead.

1. 2025 Macroeconomic Performance and Structural Policy Shifts

As of late December 2025, the Malaysian plantation sector has reached a historic inflection point, transitioning from a post-pandemic recovery phase into a new era defined by rigorous regulatory compliance and high-value diversification.

While global outlooks remained complex, domestic indicators proved robust with government GDP projections holding steady at the 4.5%–5.5% range. The agricultural sector was a primary driver of this resilience, growing faster than its 2024 rate of 3.1% due to sustained oil palm yields and a surge in high-value agro-exports.

The national economy proved resilient throughout the year, with Gross Domestic Product (GDP) projected to grow between 4.5% and 5.5%, bolstered by an agricultural sector that consistently exceeded growth expectations. To maintain liquidity amidst a softening external outlook, Bank Negara Malaysia adopted an accommodative stance by lowering the Overnight Policy Rate to 2.75% in mid-2025. Within this stable macroeconomic environment, Crude Palm Oil (CPO) prices defied early bearish forecasts to trade firmly above the RM4,000 per tonne psychological threshold as the year concluded.

A defining narrative for 2025 was the fundamental reset of the industry’s cost base, driven by the implementation of a new national minimum wage. Effective 1 February 2025, for all major listed conglomerates, the statutory minimum wage rose from RM1,500 to RM1,700, representing a 13.3% increase designed to align pay with the rising cost of living. Because labor accounts for 30% to 40% of total production costs, this mandate directly impacted 2025 operating expenditures, with analysts projecting a net earnings erosion of 1.5% to 4.1% for pure upstream players. While a second phase of implementation for micro-enterprises began in August 2025, the primary cost shock was realized early in the year by the sector’s largest employers.

Despite these rising costs, the industry avoided a more severe earnings collapse through critical policy offsets finalized during the year. Earnings erosion from the RM1,700 minimum wage hike was neutralized by critical policy offsets: a capped 2% EPF rate for foreign workers—avoiding a feared 12%–13% parity—and a RM150/tonne increase in the Windfall Profit Levy (WPL) price threshold. This structural adjustment allowed planters to retain a larger share of revenue during high-price cycles to fund the 13.3% wage increase.

The immediate enforcement of the EUDR on 30 December 2025 requires geolocation coordinates for every plot; as a ‘standard risk’ country, Malaysia faces due diligence checks on 3% of consignments, which could trigger logistical bottlenecks in Q1 2026. This looming deadline forced an industry-wide acceleration of digitization and traceability efforts, requiring exporters to provide geolocation coordinates for every plot of land in their supply chain. While large conglomerates have largely achieved compliance through systems like MSPO Trace, the end of 2025 remains a critical period of uncertainty for smallholders who risk exclusion if they cannot meet these new transparency standards. This convergence of statutory cost increases and global regulatory shifts has reshaped the Malaysian plantation landscape into a compliance-heavy but profitable environment entering 2026.

2. Oil Palm: Stability in Volatility

The Malaysian oil palm sector demonstrated remarkable price resilience throughout 2025, successfully decoupling from the volatility seen in other commodities like crude oil. Despite initial bearish forecasts from analysts, Crude Palm Oil (CPO) prices strengthened significantly in the fourth quarter, with spot prices reaching approximately RM4,035 to RM4,100 per tonne by late December. This price strength was primarily underpinned by stagnant global supply and Indonesia’s aggressive B40 biodiesel mandate, which removed substantial export volumes from the global market. While national production faced early headwinds from weather anomalies and biological stress—resulting in an 8.8% year-on-year decline in the first two months—a yield recovery in Peninsular Malaysia later in the year helped offset production dips in Sabah and Sarawak.

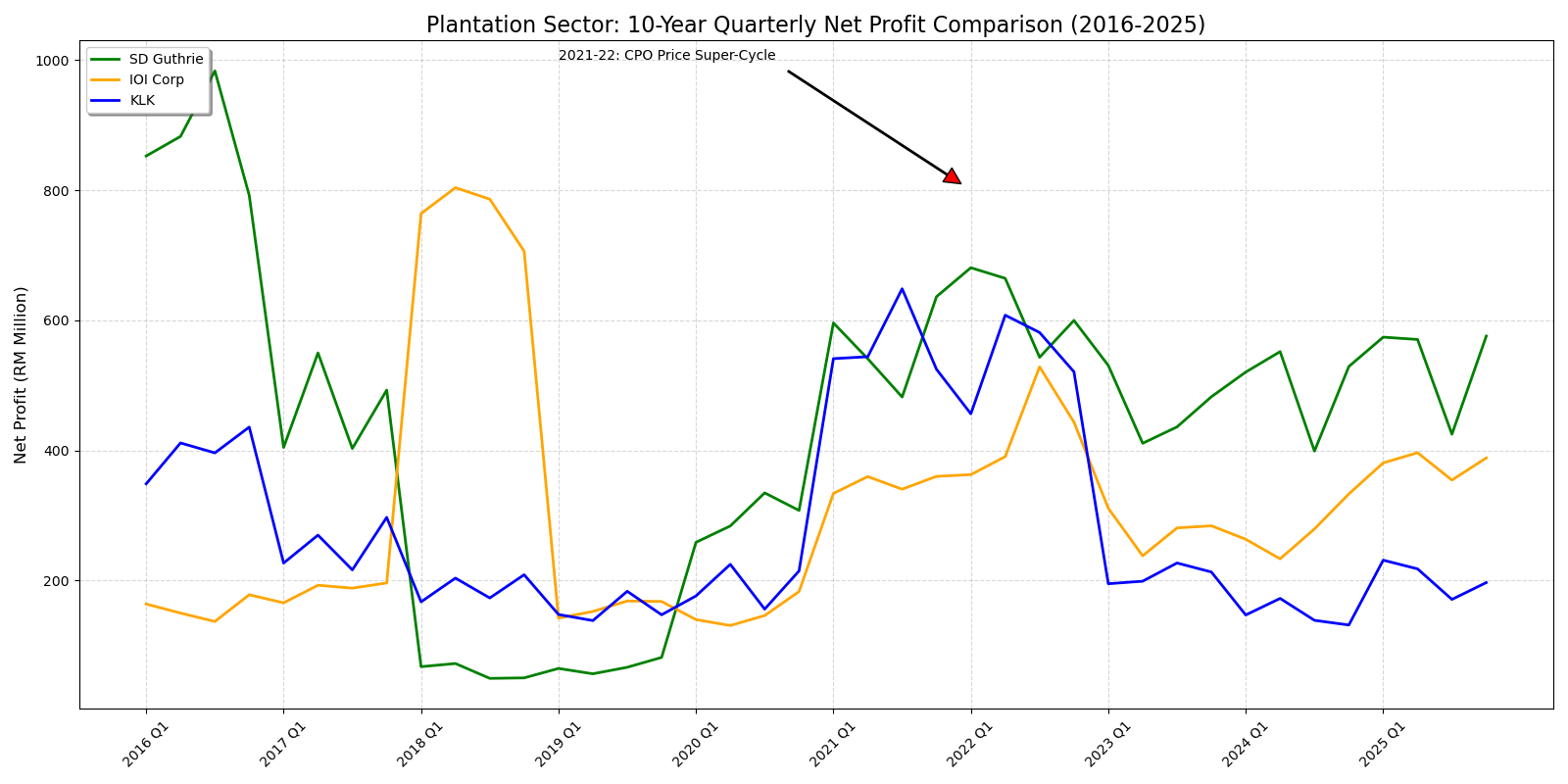

The financial results for the 2025 fiscal year highlighted a successful period for the sector’s major players, though it also revealed a divergence between upstream efficiency and downstream margin pressures. SD Guthrie’s ‘land-as-an-asset’ strategy outperformed by realizing an average CPO price of RM4,146 per tonne in Q2 FY2025, significantly higher than the previous year. This operational alpha, combined with the rollout of solar farms in Perak, allowed the company to report RM2.145 billion in net profit for the first nine months of the year.

IOI Corporation and Kuala Lumpur Kepong (KLK) also reported robust growth in their FY2025 financials. IOI Corporation’s net profit rose to RM1.52 billion from RM1.11 billion in FY2024, supported by higher Fresh Fruit Bunch (FFB) production and the resilience of its specialty fats division, which helped cushion the impact of volatile refining margins. KLK posted a net profit of RM817.27 million, a significant increase from the RM590 million recorded in the previous year. However, KLK continued to face challenges in its European oleochemical operations due to high energy costs and weak demand, necessitating a strategic pivot toward higher-value specialty ingredients through its joint venture with AAK AB.

3. Durian: The New Export Powerhouse

The durian sector transitioned into a corporate-grade export engine in 2025, with fresh fruit shipments alone exceeding RM50 million in value by mid-year following the August 2024 GACC approval. Total trade to China—encompassing fresh, frozen, and pulp—reached approximately RM150 million (US$33.9 million) in the first eleven months of 2025. Total trade to China—encompassing fresh, frozen, pulp, and paste—reached approximately US$33.9 million (roughly RM150 million) in the first eleven months of 2025. While Malaysia’s 1.44% share of China’s total durian import market remains small compared to regional competitors, the industry has successfully dominated the “ultra-premium” price bracket by positioning varieties like Musang King and Black Thorn as luxury goods.

The fundamental investment case for the sector rests on superior unit economics, often referred to as the “Green Gold” valuation. Realized trade statistics confirm a stark divergence between traditional crops and this new frontier, with mature durian orchards commanding per-hectare revenues up to nine times that of oil palm. Specifically, a hectare of mature Musang King can generate approximately RM155,000 annually compared to roughly RM17,500 for oil palm, a 9x revenue multiple that serves as the primary driver for land conversion. Furthermore, durian farming offers a higher degree of labor efficiency; despite the precise care required for the trees, it is less physically demanding during harvest, with one worker capable of managing six to eight hectares of flat land. This efficiency makes the sub-sector significantly more resilient to the statutory RM1,700 minimum wage hike than the foundational palm oil industry.

Corporate execution of this strategy remains in a capital-intensive phase characterized by long gestation periods for maturing orchards. PLS Plantations, a key proxy for the industry, reported a quarterly revenue of RM32.4 million but faced a full-year pre-tax loss of RM17.2 million due to heavy upfront development costs as it transitions its revenue recognition toward its own orchards. Meanwhile, institutional acceptance of the crop is widening as major plantation players diversify their portfolios to hedge against cyclical commodity risks. For example, IOI Corporation is actively targeting the planting of 200 hectares of durian by 2025, while FGV Holdings has finalized joint ventures to develop the crop on nearly 1,400 hectares of marginal land.

4. Industrial & Specialty Commodities: Diversified Growth in Rubber, Timber, and Niche Crops

In late 2025, Malaysia’s rubber sector experienced a stark “price boom, production bust” dynamic. While SMR 20 prices rallied to approximately 180.5 US cents per kg (roughly RM7.30–RM7.50/kg) by December due to severe supply shortages in Thailand and Indonesia, domestic upstream production continued to shrink, recording a 12.8% year-on-year decline as of August 2025. This contraction has left the sector almost entirely dependent on imports to sustain its downstream glove and tire manufacturing industries. Conversely, the timber industry remained robust, with exports valued at approximately RM22.9 billion in 2024 and an ongoing push toward a RM28 billion target. Despite facing a steep compliance curve for the European Union Deforestation Regulation (EUDR), the timber outlook for 2026 is bolstered by steady demand from the U.S. housing market and a recovery in furniture orders.

Niche agribusiness commodities, specifically cocoa and pepper, also emerged as high-performers within the national export portfolio. Malaysia has solidified its status as a global cocoa processing giant; driven by record-high global bean prices exceeding RM20,000 per tonne, export earnings reached RM12.09 billion in the first ten months of 2024 alone. The Malaysian Cocoa Board expects these earnings to surpass RM15 billion by the conclusion of 2025 and entering 2026. Simultaneously, the pepper market entered a significant “bull run,” with black pepper prices soaring 51% in 2025 to over RM27,000 per tonne. This price action propelled export values up 24% to RM186.67 million in 2024, with strong upward momentum continuing through late 2025.

5. 2026 Strategic Outlook: Valuation, Themes, and Risk Assessment

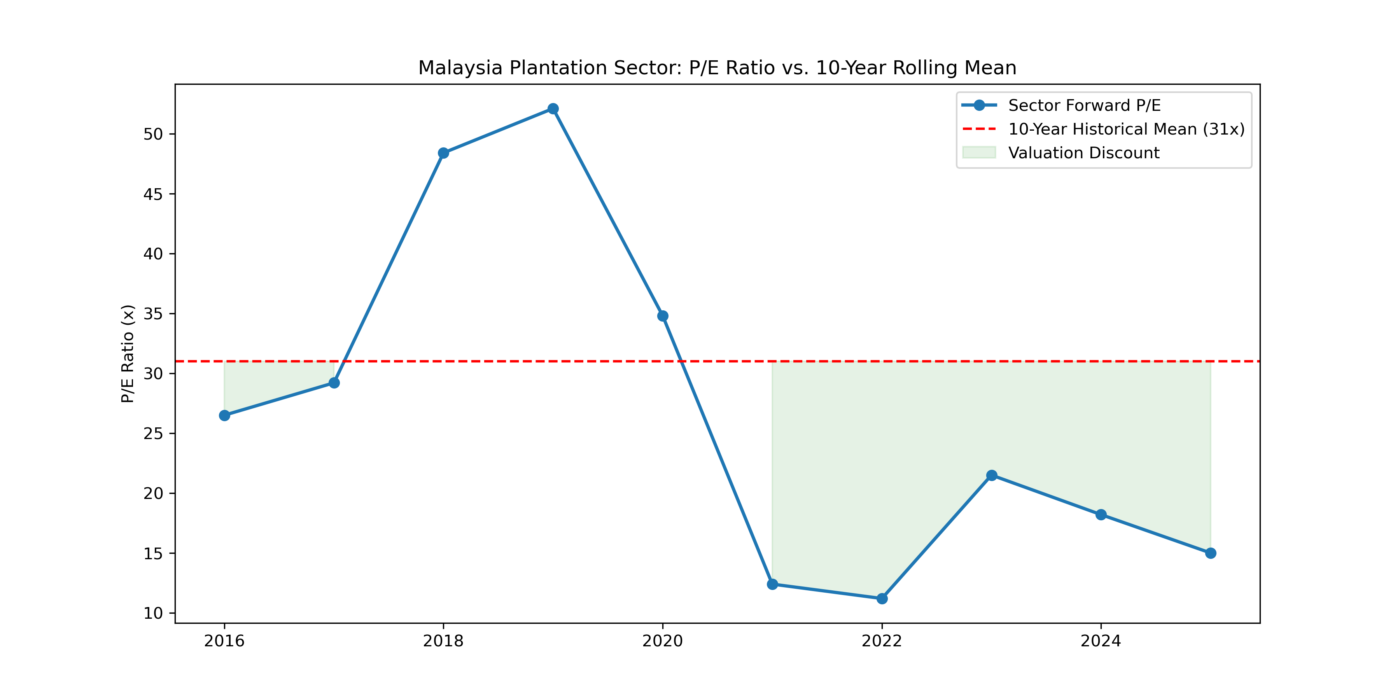

Entering 2026, the sector trades at a forward P/E of ~15x—a significant 50% discount to its 10-year mean of 31x. This valuation effectively prices in ESG and labor risks while potentially overlooking the ‘Durian Premium’ and the structural CPO price floor established above RM4,000.

The investment landscape for 2026 is defined by three distinct themes tailored to varying risk appetites. For conservative investors seeking defensive yields and safety, integrated market leaders like SD Guthrie and IOI Corporation remain the primary focus. These entities benefit from strong cash flows and high mechanization rates that help neutralize wage inflation, providing a critical buffer against potential price volatility. Conversely, companies such as PLS Plantations and FGV Holdings offer exposure to “Growth Alpha” through the high-margin durian trade. While profitability for these ventures is often deferred as orchards reach maturity, they offer significant upside for those betting on the long-term expansion of the fresh fruit export market. For investors seeking direct sensitivity to the sustained high-price environment, pure upstream players are favored for their immediate exposure to current commodity cycles.

Despite this positive momentum, several key risks warrant close monitoring in the first half of 2026. The immediate enforcement of the European Union Deforestation Regulation (EUDR) at the end of 2025 could trigger logistical bottlenecks and administrative hurdles at European ports during the first quarter of the new year. Furthermore, the potential for new international trade tariffs presents an indirect threat to commodity demand by potentially slowing global trade cycles. Finally, meteorological forecasts suggest a potential La Niña event in 2026; while such weather patterns typically disrupt harvesting and lower production volumes, they often act as a price catalyst by creating supply anxieties in the global edible oil market. As 2025 concludes, the sector is well-positioned for a profitable, albeit compliance-heavy, 2026.