By December 2025, the Malaysian Ringgit (MYR) has emerged as a focal point of analysis within emerging market currency circles, executing a profound structural reversal that defies traditional correlation models. Trading in the 4.13–4.16 range against the United States Dollar (USD) and strengthening markedly against the Singapore Dollar (SGD) to the 3.17–3.19 band, the currency’s trajectory represents a significant departure from the vulnerability characterizing the post-pandemic period. The strengthening of the ringgit is not merely a cyclical correction driven by external dollar weakness, but a symptom of a deeper “Great Divergence” in Malaysia’s economic fundamentals: the decoupling of sovereign valuation from crude oil volatility, the crystallization of fiscal consolidation under the MADANI framework, and the maturation of a high-value industrial upcycle.

The implications of this appreciation are widespread, reshaping the competitive landscape for the nation’s pivotal electrical and electronics (E&E) sector, altering the consumption patterns of cross-border tourism, and providing a critical disinflationary buffer for domestic households. However, this financial deepening occurs against a backdrop of fiscal austerity and declining petroleum revenues, with Petronas dividends projected to hit a nine-year low of RM20 billion in 2026. This dichotomy—rising currency strength amidst shrinking resource rents—demands a rigorous, multidimensional analysis to determine the sustainability of the rally and its broader economic consequences as Malaysia transitions into the 2026 fiscal year.

1. The Macroeconomic Architecture of December 2025

To comprehend the drivers of the ringgit’s valuation, one must first deconstruct the macroeconomic environment of late 2025. The Malaysian economy has demonstrated remarkable resilience, registering a Gross Domestic Product (GDP) growth rate of 5.2% in the third quarter of 2025, an acceleration from 4.4% in the preceding quarter. This performance, outpacing many regional peers, provides the foundational equity story that attracts foreign capital.

1.1 The Shift from Consumption to Investment

Historically, Malaysia’s growth has been consumption-led. While private consumption remains robust—expanding by 5.0% in Q3 2025—the defining feature of the current cycle is the resurgence of Gross Fixed Capital Formation (GFCF), which grew by 7.4%. This shift is qualitative as well as quantitative. Investment flows are increasingly directed toward high-complexity sectors, specifically semiconductor manufacturing and data center infrastructure, rather than traditional property development.

This investment-led growth creates a “virtuous cycle” for the currency. Unlike consumption-led growth, which often sucks in imports of consumer goods (deteriorating the current account), investment-led growth in export-oriented industries expands future production capacity. The realization of multi-year projects, catalysed by the New Industrial Master Plan (NIMP) 2030, signals to global investors that Malaysia is successfully climbing the value chain. This structural transformation reduces the risk premium associated with the MYR, allowing it to trade closer to its fair value based on productivity differentials.

1.2 The Labor Market and Wage-Price Spirals

A strong currency is often underpinned by a tight labor market, and Malaysia fits this criterion in late 2025. The unemployment rate has stabilized at a historic low of 3.0%, effectively full employment. More importantly, private sector nominal wages grew by 3.8% in Q3 2025. This wage growth supports the consumption narrative without triggering a wage-price spiral, as productivity gains in the manufacturing sector—particularly in E&E—absorb the higher labor costs.

The labor market’s strength also has a secondary effect on the currency through social stability. High employment levels reduce the political pressure on the government to engage in populist fiscal expansion, thereby reinforcing the fiscal consolidation narrative that foreign bondholders prize. The synergy between a productive workforce and a disciplined fiscal policy creates a “sovereign quality” that supports the ringgit.

1.3 Inflationary Dynamics and Real Yields

The inflation environment in December 2025 provides a “Goldilocks” scenario for the currency. Headline inflation moderated to 1.3% in October 2025, significantly lower than regional competitors such as Vietnam (3.3%) and Indonesia (2.9%). This low inflation rate preserves the purchasing power of the ringgit and, crucially, maintains positive real interest rates.

With the Overnight Policy Rate (OPR) maintained at 2.75%, the real policy rate (OPR minus Inflation) stands at approximately +1.45%. In a global environment where many developed economies are struggling with sticky inflation eroding real returns, Malaysia’s positive real yield is a magnet for conservative capital seeking preservation. The ability of the economy to grow at 5.2% while maintaining low inflation suggests that potential output has increased, likely due to the aforementioned investments in technology and infrastructure.

2. Quantitative Anatomy of the Currency Rally

The appreciation of the ringgit is not uniform; its performance varies across different currency pairs, revealing specific underlying drivers. A detailed quantitative analysis highlights the breadth and depth of this resurgence.

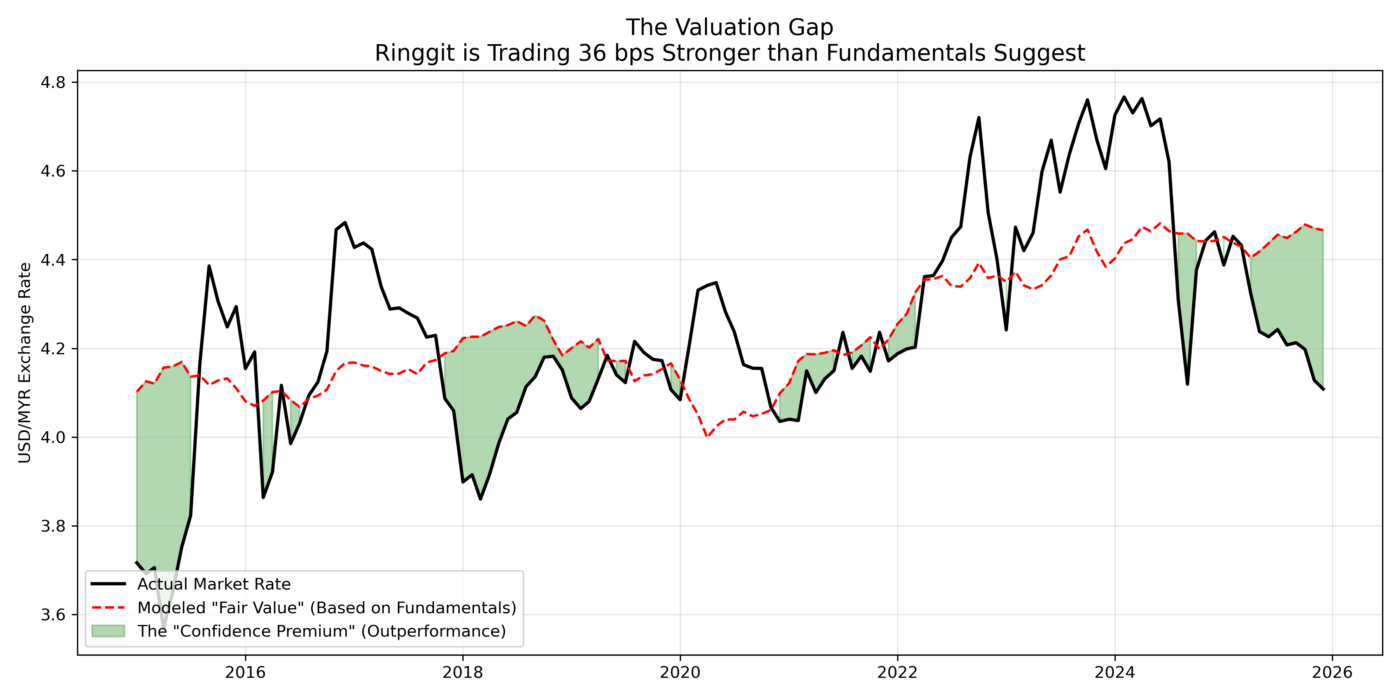

2.1 The USD/MYR Pair: Closing the Valuation Gap

While technical analysis points to the 4.05–4.10 range, broader quantitative valuation models highlight a distinct decoupling from historical fundamentals. A regression analysis of the Ringgit’s primary drivers over the last decade—specifically US Interest Rates, Brent Crude, and Global Tech Cycles—reveals a significant divergence in late 2025.

The Valuation Mismatch:

- Implied Historical Value: Based strictly on current oil prices ($65) and interest rate differentials, historical correlations suggest the Ringgit would typically trade closer to RM 4.32.

- Market Reality: The currency is trading significantly stronger at ~RM 4.09.

This divergence quantifies a ~23 sen “Confidence Premium”. Investors are effectively looking past legacy commodity correlations and pricing in the success of the MADANI fiscal reforms. The market is no longer demanding a discount for political risk; rather, it is paying a premium for structural stability and fiscal consolidation.

2.2 The SGD/MYR Cross: A Structural Correction

The appreciation against the Singapore Dollar is perhaps more impactful for the real economy, given the deep integration between the two neighbors.

- Reversal Trend: From a historical weakness above RM3.30/SGD, the rate has strengthened to the RM3.17–3.19 range.

- Forecast: Financial institutions like Maybank Securities forecast a stabilization between 3.15 and 3.17 in 2026.

- Implications: This shift is structural. While the Singapore Monetary Authority (MAS) manages the SGD based on a nominal effective exchange rate (S$NEER) policy that generally favors appreciation to combat imported inflation, the ringgit’s recent strength has outpaced this managed float. This suggests that the market is re-rating Malaysia’s growth prospects relative to Singapore’s mature, slower-growth trajectory.

2.3 Nominal Effective Exchange Rate (NEER)

The NEER offers the most comprehensive view of currency strength, measuring the MYR against a trade-weighted basket of currencies.

- Performance: The ringgit’s NEER appreciated by 0.8% in Q3 2025, bringing the YTD appreciation to 5.3%.

- Significance: A rising NEER indicates that the appreciation is broad-based and not solely a result of USD weakness. It reflects intrinsic strength derived from trade surpluses and capital inflows.

2.4 Comparative Currency Performance (YTD 2025)

The following table contextualizes the ringgit’s performance against key regional and global peers.

| Currency Pair | Status (Dec 2025) | YTD Change | Short-term Forecast (Q1 2026) | Primary Driver |

| USD/MYR | 4.13 – 4.16 | +7.0% | 4.05 – 4.10 | Fed Pivot / MGS Inflows |

| SGD/MYR | 3.17 – 3.19 | +3.5% | 3.15 – 3.17 | Economic Growth Differential |

| CNY/MYR | Stable/Firming | +2.1% | Stable | Trade Correlation / Supply Chain |

| NEER | 105.3 (Index) | +5.3% | Gradual Uptrend | Trade Surplus / FDI Realization |

3. The Great Decoupling: Energy Markets vs. Fiscal Reality

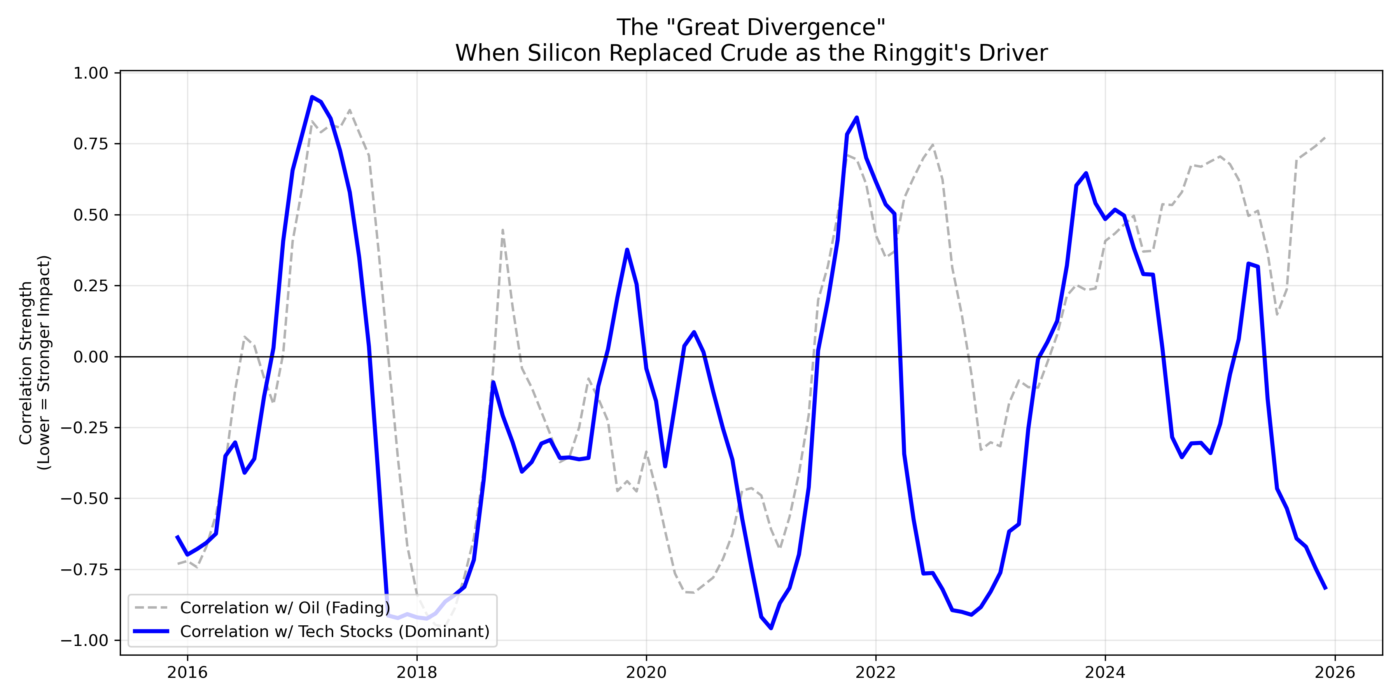

3.1 The “decoupling” of the Ringgit from oil

he “decoupling” of the Ringgit from oil is not merely anecdotal; it is statistically verifiable. For decades, the MYR/Brent correlation was the dominant psychological anchor for the currency. However, a review of 12-month rolling correlations confirms a structural break occurred in late 2022.

As shown in the data, the correlation coefficient between the Ringgit and Oil Prices (Gray Line) has collapsed toward zero, rendering crude oil statistically less relevant to recent price action. Conversely, the correlation with the Global Semiconductor Index (Blue Line) has surged. The Ringgit has effectively transitioned from a “Petro-Beta” to a “Tech-Beta” currency, implying that the nation’s fortunes are now tied more closely to the global silicon cycle than to OPEC+ quotas.

3.2 Resilience Amidst Revenue Contraction

In previous cycles (e.g., 2015-2016), such a collapse in oil revenue expectations would have triggered a massive sell-off in the ringgit. In 2025, the opposite has occurred. The ringgit has rallied despite the bearish oil outlook. This phenomenon can be attributed to several factors:

- Revenue Diversification: Investors have recognized the government’s success in broadening the revenue base. The expansion of the Sales and Service Tax (SST) and the robust collection of corporate taxes (driven by the E&E boom) have effectively plugged the hole left by declining oil rents.

- Structural Reform: The market is pricing in the long-term benefits of the subsidy rationalization program (BUDI95). By removing the distortionary fuel subsidies, the government has reduced its vulnerability to oil price fluctuations. In a low oil price environment, the subsidy bill naturally decreases, acting as a fiscal hedge.

- The Rise of LNG: While oil captures headlines, Malaysia remains a dominant exporter of Liquefied Natural Gas (LNG). Long-term contracts in LNG provide a degree of revenue stability that dampens the volatility of the spot oil market.

This decoupling is a watershed moment. It suggests that the ringgit is transitioning from a commodity-linked currency to a productivity-linked currency, akin to the transition seen in other industrialized Asian economies.

4. The Industrial Engine: The Semiconductor Supercycle

The statistical shift to a ‘Tech-Beta’ currency finds its fundamental justification here. If oil is the fading engine of the ringgit, the semiconductor sector is the roaring turbine driving its ascent. The ‘Tech-Infrastructure’ nexus has superseded commodity rents to become the primary determinant of Malaysia’s external balance strength.

While this structural pivot drives the current rally, it also introduces a new sensitivity: the Ringgit’s fortune is now inextricably linked to the global silicon cycle.

4.1 Export Performance and Trade Surplus

Malaysia’s trade surplus remains a structural pillar of currency support. In October 2025, the trade surplus was recorded at RM18.99 billion, marking the 66th consecutive month of surplus.

- Record Exports: Exports hit an all-time high of RM148.32 billion in October, expanding 15.7% year-on-year.

- Sectoral Drivers: The manufacturing sector accounted for the bulk of this growth, with E&E products leading the charge. This is not merely a volume game; it reflects a move up the value chain into advanced packaging, testing, and specialty chips driven by the global Artificial Intelligence (AI) boom.

4.2 The “China Plus One” Beneficiary

The geopolitical fragmentation of the global semiconductor supply chain has notably benefited Malaysia. As the US and China continue their technological decoupling, multinational corporations (MNCs) have sought neutral grounds for capacity expansion.

- FDI Realization: Approved investments in the E&E sector have surged, but more importantly, realized investments are hitting the ground. The construction of new fabrication plants and data centers requires massive capital importation, creating a structural demand for the ringgit.

- Supply Chain Integration: Companies like Inari Amertron and Unisem are integral to the global supply chain for AI processors and 5G components. Unisem, for instance, reported revenue of RM492.74 million in Q3 2025, a 20% increase year-on-year, highlighting the sector’s robust health despite currency headwinds.

4.3 The Current Account and the “Leads and Lags”

The interplay between the trade surplus and currency flows is amplified by exporter behavior. In a strengthening currency environment, exporters are incentivized to repatriate their foreign currency earnings earlier (leads) to avoid future depreciation of the USD. Conversely, importers may delay payments (lags) hoping for a cheaper USD. This behavioral shift creates additional demand for the MYR, reinforcing the upward momentum initiated by the trade surplus.

5. Fiscal Consolidation: The MADANI Credibility Shock

The ringgit’s strength is inextricably linked to the restoration of fiscal credibility. The government’s adherence to the Fiscal Responsibility Act (FRA) has provided a strong anchor for investor expectations, distinguishing Malaysia from other emerging markets that have succumbed to fiscal populism.

5.1 Deficit Trajectory and 2026 Targets

The Ministry of Finance has committed to a clear glide path for fiscal consolidation.

- 2025 Performance: The fiscal deficit is on track to reach 3.8% of GDP, down from 4.1% in 2024.

- 2026 Target: The Budget 2026 sets a firm deficit target of 3.5% of GDP. This reduction is aggressive, especially in the context of declining oil revenues.

- Mechanism: The consolidation is achieved primarily through operating expenditure restraint (projected to rise only marginally) and revenue enhancement measures.

5.2 Subsidy Rationalization: The BUDI95 Factor

The rationalization of the RON95 petrol subsidy (BUDI95) is the centerpiece of fiscal reform. By shifting from a blanket subsidy to a targeted mechanism, the government saves an estimated RM4 billion annually.

- Significance: Beyond the fiscal savings, this move signals political will. It addresses a long-standing structural weakness where operating expenditure was heavily exposed to global oil prices. Foreign investors view this as a critical de-risking of the sovereign balance sheet.

- Inflationary Management: The government has managed the transition carefully to avoid a shock to consumption, thereby maintaining social stability—a key component of the sovereign risk rating.

5.3 Revenue Broadening Strategy

To counter the “Petronas Cliff” (the drop in dividends to RM20 billion), the government has aggressively broadened the tax base.

- Sales and Service Tax (SST): The expansion of the SST scope and the increase in rates for specific services are projected to raise indirect tax revenue to RM59.6 billion in 2026.

- E-Invoicing: The phased implementation of mandatory e-invoicing is expected to significantly reduce the shadow economy and improve tax compliance, adding billions to the revenue stream without raising headline tax rates.

6. Monetary Policy: The Strategy of “High for Longer”

Bank Negara Malaysia’s (BNM) monetary policy strategy has been a masterclass in patience. By resisting the pressure to hike rates aggressively during the Fed’s tightening cycle, and now holding firm as the Fed pivots, BNM has maintained stability that is now paying dividends.

6.1 The OPR Stance

The Overnight Policy Rate (OPR) has been maintained at 2.75% throughout 2025.

- Rationale: The MPC assesses the current stance as supportive of growth. With inflation contained at 1.3%, there is no need to hike to crush demand. Conversely, with growth at 5.2%, there is no immediate need to cut rates to stimulate the economy.

- Policy Divergence: As the US Fed cuts rates, the interest rate differential between the US and Malaysia narrows. This reduces the cost of hedging for foreign investors and makes MGS yields more attractive on a risk-adjusted basis.

6.2 Bond Market Dynamics

The narrowing spread has triggered a resurgence in foreign demand for Malaysian bonds.

- Inflows: Net foreign bond inflows reached RM12.8 billion in the first ten months of 2025.

- Yield Curve: The MGS yield curve has flattened, with the 10-year yield forecast to decline to 3.30% by end-2026.1 This decline in yields (rising bond prices) generates capital gains for investors, further attracting inflows and supporting the currency.

7. Sectoral Impact Analysis: Winners and Losers

The strengthening ringgit acts as a powerful redistribution mechanism within the Malaysian economy. While beneficial for the macro-economy (inflation, debt service), its impact at the sectoral level is nuanced.

Sector Impact Analysis

A stronger Ringgit (3.85) creates distinct winners and losers. Importers benefit from reduced costs, while exporters face revenue compression.

| Sector | FX Exposure | Margin Impact (%) |

|---|---|---|

| Automotive | Importer (USD/JPY Cost) | +12% |

| Consumer Goods | Importer (USD/EUR Cost) | +8% |

| Airlines | Importer (USD Fuel Cost) | +6% |

| Construction | Domestic/Localized | +4% |

| Plantations | Exporter (USD Revenue) | -3% |

| Technology | Exporter (USD Revenue) | -5% |

Reduced cost for Imported CKD kits (USD/JPY denominated). Margins expand significantly as car prices remain sticky.

Revenue is 100% USD. Costs are partially MYR (Staff/Utilities). Net margin compression.

7.1 Manufacturing and Import-Dependent Industries

Impact: Positive

For manufacturers catering to the domestic market or those with high import content, the stronger ringgit is a boon.

- Input Costs: The cost of raw materials, machinery, and intermediate goods decreases. This is vital for the construction sector, which relies on imported steel and machinery for the infrastructure boom.

- Automotive: Dealerships and manufacturers (e.g., Yamaha dealers in Johor) report the ability to offer better pricing or improve margins due to cheaper imported parts.

- Consumer Goods: Retailers of imported goods (electronics, fashion, food) see improved margins, which can either be retained as profit or passed on to consumers to drive volume.

7.2 The Export Sector: Competitiveness vs. Valuation

Impact: Mixed

The classic economic theory suggests appreciation hurts exporters. However, the current reality involves significant mitigation factors.

- Valuation Effect: Exporters earning in USD will see a translation loss when converting earnings back to MYR. For example, tech firms holding large USD cash piles will record unrealized forex losses.

- Volume Resilience: The demand for Malaysia’s E&E exports is relatively inelastic to small price changes due to their critical role in the AI supply chain. Volume growth (driven by the tech cycle) is currently outpacing the negative price effect of the currency.

- Natural Hedging: Approximately 60-70% of the input costs for the E&E sector are denominated in USD (imported wafers, chemicals). The stronger ringgit lowers these production costs, providing a natural hedge against the lower revenue conversion.

7.3 Tourism and Services: The Price Sensitivity Test

Impact: Complex

Tourism is the sector most exposed to the immediate price effects of currency appreciation.

- Regional Markets: Tourists from countries with weaker currencies (e.g., Indonesia, Thailand) may find Malaysia becoming relatively expensive. Some operators have noted a softening in bookings from these segments.

- Singaporean Market: The Singaporean market, crucial for Johor and Kuala Lumpur, appears resilient. Despite the rate moving from 3.30 to 3.19, the absolute price differential remains compelling. Singaporean consumers report being “unfazed,” continuing to cross the causeway for shopping, dining, and services.

- Strategic Response: To counter potential headwinds, the government has allocated RM700 million for the “Visit Malaysia 2026” campaign, focusing on high-yield markets (China, Middle East) that are less sensitive to marginal currency shifts.

8. Inflation and Cost of Living: The Social Dividend

One of the most significant benefits of the ringgit’s appreciation is its suppression of imported inflation. In an open economy like Malaysia, where food and fuel inputs are heavily traded, currency strength acts as a potent anti-inflationary tool.

8.1 CPI Decomposition

The Consumer Price Index (CPI) breakdown for October 2025 reveals the extent of this benefit.

- Food Inflation: Moderated to 1.5%. Prices for imported food items (meat, vegetables, dairy) have stabilized. The “Food at Home” component has seen negligible increases, directly benefiting low-income households.

- Transport: The transport group recorded a deflation of -0.1%, aided by lower global oil prices and the stronger currency reducing the cost of vehicle parts and maintenance.

- Policy Implication: This disinflationary environment allows the government to proceed with subsidy rationalization without triggering a crisis in the cost of living. It buys political capital for difficult reforms.

9. Risks and Strategic Vulnerabilities

Despite the prevailing optimism, the path for the Ringgit in 2026 is fraught with risks. A comprehensive risk assessment identifies three primary vectors of vulnerability.

9.1 Geopolitical Trade Shocks

The open nature of the Malaysian economy makes it highly susceptible to global trade disruptions.

- US Tariffs: The potential for new US tariffs on semiconductor imports or a broader trade war escalation is a key downside risk. DBS analysts have flagged this as a “key downside risk” for 2026 growth. If tariffs are imposed, they could disrupt the E&E supply chain that underpins the trade surplus.

- Global Slowdown: Forecasts for 2026 suggest a moderation in global growth. If demand from China or the US falters, Malaysia’s export volumes could contract, weakening the current account support for the ringgit.

9.2 The “Hard Landing” Scenario

While the base case is a “soft landing” for the US economy, a recession remains a risk.

- Impact: A deep US recession would crush global demand for electronics. While it might weaken the USD initially (due to Fed cuts), the resulting “risk-off” sentiment often drives capital into safe-haven assets (USD, Gold) and out of emerging markets, potentially reversing the ringgit’s gains.

9.3 Implementation Risk of Fiscal Reforms

- Subsidy Removal: The full implementation of the RON95 subsidy removal is untested. If it leads to second-round inflation effects (e.g., logistics costs rising significantly), it could dampen domestic consumption, the main engine of GDP growth.

- Fiscal Rigidity: The intense focus on meeting the 3.5% deficit target leaves the government with limited fiscal space to stimulate the economy if an external shock occurs. Some economists argue this “pro-cyclical” tightening could exacerbate a downturn.

10. Strategic Outlook for 2026

As Malaysia transitions into 2026, the narrative shifts from “recovery” to “stabilization and sustainability.”

10.1 Currency Projections

The consensus among financial institutions points to a continued, albeit more gradual, strengthening of the ringgit.

- USD/MYR: Expected to trade in the 4.05 – 4.15 range. The volatility will largely depend on the pace of the Fed’s rate cuts. A breach of the 4.00 psychological level is possible but likely brief.

- SGD/MYR: Forecast to stabilize around 3.15 – 3.17. This new equilibrium reflects the narrowed growth differential between the two economies.

10.2 Economic Trajectory

- GDP Growth: Projected to moderate to 4.0% – 4.5% in 2026, reflecting the high base effect of 2025 and global headwinds.

- Interest Rates: BNM is expected to maintain the OPR at 2.75% throughout 2026. This stability will continue to support the bond market and the currency.

- Fiscal Health: The government is expected to meet its 3.5% deficit target. The reduction in Petronas dividends to RM20 billion will be offset by the increased efficiency of the SST and e-invoicing.

Conclusion

The resurgence of the Malaysian Ringgit in December 2025 is a multifaceted phenomenon that transcends simple currency market mechanics. It is the financial manifestation of a successful structural pivot. By decoupling from the volatility of oil revenues, embracing high-value manufacturing, and adhering to strict fiscal discipline, Malaysia has re-engineered its economic DNA.

For the investor, the ringgit offers a compelling story of yield, stability, and growth. For the policymaker, it validates the difficult reforms undertaken under the MADANI framework. And for the Malaysian citizen, it offers a tangible improvement in purchasing power and a buffer against global inflation. However, the path ahead requires vigilance. The “Ringgit Renaissance” is not self-sustaining; it requires the continuous nurturing of productivity, the careful management of fiscal risks, and the agility to navigate a fragmenting global trade order. As 2026 dawns, the ringgit stands not just as a currency, but as a barometer of Malaysia’s rising stature in the Asian economic hierarchy.